Insights

The Regulatory Landscape for Digital Assets: What’s Next?

Insights

The Regulatory Landscape for Digital Assets: What’s Next?

Since the first Bitcoin transaction in January 2009, digital assets have come a long way from the fringes of finance to a $3 trillion¹ asset class and a focal point of investor and regulatory attention. Ownership of digital assets has risen at an exponential pace, from only 5 million users in 2016 to over half a billion currently, with daily transaction volumes topping $400 billion a day² in January. Blockchain technology, initially viewed with skepticism by institutional investors as a novelty with still unknown utility, is now being rapidly integrated into mainstream financial markets thanks to rising digital asset prices, increased transparency, and new product launches.

With strong investor demand and increasing adoption, governments worldwide have had to respond to the needs of an emerging market needing laws and guidelines that foster innovation, while ensuring consumer protection. The year 2024 has been a landmark in this regulatory evolution - from the EU’s Markets in Crypto-Assets Regulation (MiCA), to President Trump’s Working Group on Digital Asset Markets, major jurisdictions are not only legitimising digital assets, but paving the way for large scale institutional adoption. With Bitcoin breaking the $100,000 barrier for the first time, and over 560 million people owning digital assets worldwide, 2025 is building on this momentum. By the end of 2025, 861 million users3 are expected to own digital assets, over 10% of the world’s population.

For the world’s 23 million⁴ high-net-worth individuals (HNWIs) and global $145 trillion⁵ wealth management sector, regulatory clarity in investments is not an option, but absolutely fundamental. Fiduciary duties towards clients and custodial integrity remain the top priorities for the global asset management industry, embedded in legislation and enforced by financial regulators. Unsurprisingly, it is a lack of regulatory clarity that has been cited for years as the number one hurdle⁶ stopping HNWIs, financial advisers, and asset managers from investing in digital assets - despite a tremendous interest in doing so.

A 2024 survey by EY-Parthenon revealed that nearly all institutional investors (94%⁷) believe in the long-term value of digital assets and blockchain technology. Investors have also been attracted by the significant returns generated by digital assets, with Bitcoin (BTC) and Ethereum (ETH), up 125% and 45% respectively in 2024, compared to 27.6% for the S&P 500. An index of digital asset prices between 2017 and 2024 outpaced the returns of a portfolio of global stocks by a factor of over 5:1⁸ and with a higher Sharpe ratio⁹. Furthermore, the low correlation levels of digital assets to other asset classes has significantly improved the performance of institutional portfolios integrating a digital asset component, independently from the portfolio’s starting date¹⁰.

As a result, the number of institutional investors holding at least some digital assets has risen from less than 10%¹¹ in 2019 to over 37%¹² today. The size of allocations is also projected to increase, from an estimated 1%-3% of institutional portfolio values currently to 7.2% by 2027¹³. Furthermore, 70% of institutional investors¹⁴ plan to increase their exposure to digital assets in the next 2-3 years.

As institutional investor appetite for digital assets has risen, the financial sector has responded with a number of products to cater to it. After the launch of the first Bitcoin ETP in 2013, followed by derivative product launches on the CBOE and CME exchanges in 2017, January 2024 witnessed the launch of the first US spot bitcoin ETF¹⁵. With digital asset financial products now a $100 billion+ AuM category¹⁶, global authorities are stepping up to keep the sector secure, compliant, and ready to absorb a significantly larger influx of investor funds.

The digital asset regulatory landscape continues to evolve at different speeds across jurisdictions. While some jurisdictions have historically exhibited a highly favourable regulatory framework, notably El Salvador, the UAE, and Switzerland, others, including the US and EU, have taken a more complex stance, with a mix of restrictive and accommodating elements. In addition to managing regulation in the private sector, 134 countries¹⁷ are currently engaged in research and pilot programs for CBDCs, including 13¹⁸ out of the G20 countries. Nevertheless, the overarching trend exemplified in 2024 is one of increasing acceptance:

United States: The U.S. has seen a paradigm shift towards digital assets. The rescinding of Staff Accounting Bulletin (SAB) No 121 with No 122 in January 2025¹⁹ has opened the door for banks to explore digital asset custody services without the previously prohibitive capital requirements. The regulatory momentum carried through into the end of 2024 with the Trump presidential campaign, characterised by very favourable pronouncements and the establishment of the Presidential Council of Advisers for Digital Assets. Days following the inauguration, President Trump issued an executive order titled “Strengthening American Leadership in Digital Financial Technology,” in a bid to make crypto a policy priority for the US economy. The SEC has also announced the formation of a Crypto Task Force²⁰ to develop a comprehensive and clear regulatory framework for crypto assets. Digital asset support has also been manifested within the legislative branch, with Sen. Lummis gathering bipartisan support for a Bitcoin reserve proposal to purchase up to one million BTC by 2030²¹. At the state level, at least 18 states²², including Arizona and Utah, are reviewing crypto reserve legislation.

European Union: The EU's Markets in Crypto-Assets Regulation (MiCA) became fully effective in December 2024, establishing a unified baseline legal framework for crypto assets across member states. MiCA aims to enhance consumer protection and transparency, requiring service providers to obtain licenses and adhere to stringent governance and regulatory standards. This regulatory cohesion is expected to bolster investor confidence, consumer protection and streamline operations within the EU's digital asset market. A number of individual member states, including Ireland²³, the Netherlands²⁴, and Germany²⁵, have also recently made public announcements regarding the need for a digital euro central bank digital currency (CBDC). Despite EU central banks not yet holding digital assets, the Czech National Bank announced a potential plan to invest up to €7 billion²⁶ of its reserves in bitcoin, equivalent to 5% of the total.

United Kingdom: The UK government introduced legislation in September 2024 to classify digital assets and NFTs as personal property under British law. This move provides legal protection and facilitates the recovery of stolen digital assets, reflecting the UK's commitment to fostering a secure environment for digital asset transactions. Furthermore, In January 2025 the Bank of England (BoE) has published an initial design note²⁷ on a blueprint for a digital pound.

Asia: Countries like Singapore and Japan continue to lead with progressive crypto regulations. Singapore's Singapore's Payment Services Act offers a comprehensive framework for digital payment token services, while Japan's amendments to its Payment Services Act and Financial Instruments and Exchange Act have strengthened oversight of crypto exchanges, ensuring robust consumer protection and market integrity. In December 2024, Hong Kong introduced the Stablecoins Bill²⁸ to establish a regulatory framework for stablecoin issuance, one of the world’s first. Other Asian countries are also showing signs of progress on the regulatory front. In South Korea, the Virtual Asset Investor Protection Act was introduced in July 2024²⁹, marking South Korea’s regulatory commitment to protecting investors and promoting the integrity of digital asset markets. This follows the Financial Services Commission’s (FSC) announced plans³⁰ to phase in the institutional trading of digital assets in H2 2025.

Middle East: The UAE in particular has positioned itself as a global digital asset hub, with Dubai’s Virtual Assets Regulatory Authority (VARA) providing what is considered one of the most comprehensive legal frameworks for digital assets in the world. Digital Assets Law N.2, enacted in March 2024³¹, provides legal clarity on the status of digital assets and established guidelines for their control and transfer The Federal Tax Authority eliminated a 5% VAT tax³² on digital assets trading and purchases in October 2024, in a bid to stimulate investment in the sector.

Latin America: In November 2024, Brazil introduced a bill³³ proposing the creation of a Sovereign Strategic Bitcoin Reserve (RESBit) to diversify the National Treasury's assets. The country is also preparing the launch of its CBDC, known as Drex³⁴, in the first half of 2025. Argentina is also establishing a comprehensive framework for virtual asset service providers (VASPs). In October 2024, the Comisión Nacional de Valores (CNV) issued a General Resolution regulating the activities and compliance needs of VASPs operating in Argentina. The continent also is home to El Salvador, the first country to make Bitcoin legal tender in 2021, and whose central bank has over 6,000 bitcoins in reserve³⁵.

With a favourable policy shift in the US and the successful launches of spot bitcoin ETFs³⁶ and ETPs³⁷ in the US and EU in 2024, it is likely that 2025 will see more successful product launches. Furthermore, the range of products introduced will likely expand to:

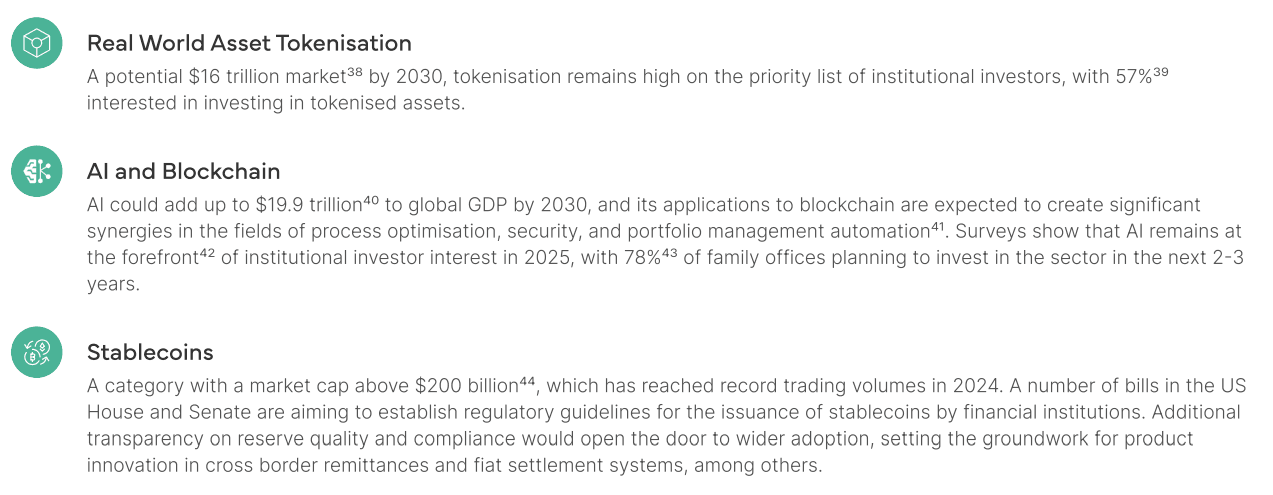

As institutional acceptance of digital assets increases, investors will look to the additional digital asset use-cases as investment opportunities, including: