Reports

Digital Asset Market - January in Review

Reports

Digital Asset Market - January in Review

January marked a transition month for markets, characterised less by new information than by a gradual repricing of risk across asset classes. In traditional markets, headline indices remained resilient, but underlying dynamics pointed to a more selective and less forgiving environment, with dispersion increasing across equities, credit and commodities. While broader financial conditions remained supportive, market reactions became increasingly sensitive to earnings quality, positioning and execution risk rather than broad narrative shifts.

At the same time, digital asset markets exhibited a distinct set of dynamics. Within crypto markets specifically, liquidity conditions softened at the margin as trading volumes and market depth declined from late-2025 levels. Leverage was reduced, and price action became more dependent on positioning, timing and market structure, particularly during periods of stress and off-peak trading hours. This divergence in market microstructure helps explain why digital assets experienced sharper, more nonlinear price moves despite the absence of a material deterioration in underlying fundamentals.

Geopolitical headlines and macro developments continued to generate episodic volatility across both traditional and digital assets, but markets largely faded rhetoric in the absence of concrete policy follow-through. Notably, the late-month sell-off in precious metals underscored how leverage and positioning can still trigger abrupt cross-asset de-risking, even when the broader macro backdrop remains intact. Digital asset markets experienced a similar dynamic, with a sharp, technically driven sell-off into month-end reflecting thinner liquidity and heightened macro sensitivity rather than a deterioration in crypto-specific fundamentals.

Overall, January reinforced an environment in which traditional assets remain supported by resilient growth and earnings, while digital assets are increasingly shaped by market structure and liquidity dynamics internal to the crypto ecosystem. In this regime, returns are driven less by broad beta exposure and more by selectivity, discipline and risk management, particularly within digital asset markets where timing and execution remain critical.

Risk assets entered 2026 with cautious optimism following a strong but increasingly narrow rally in 2025. January saw global equity markets grind modestly higher, albeit with growing dispersion beneath the surface. The S&P 500 rose by roughly 1.4% over the month, supported by resilient earnings and still-favourable liquidity conditions, while the Nasdaq 100 gained around 1.2%, underperforming slightly as mega-cap technology leadership showed early signs of fatigue. European equities lagged their U.S. counterparts, with the Euro Stoxx 50 up approximately 0.7%, weighed down by softer growth momentum and persistent fiscal uncertainty across parts of the Eurozone. Overall, headline index performance masked a more selective market environment in which stock-specific fundamentals increasingly mattered.

Markets were briefly unsettled by a bout of geopolitically driven volatility during the month, following headlines related to Greenland and renewed tit-for-tat trade rhetoric between major economies. Risk assets initially sold off, but the move was quickly retraced as investors once again applied the so-called ˝TACO trade˛ playbook, strongly discounting the likelihood that the U.S. administrationˇs threats would translate into sustained or economically meaningful escalation. As in prior episodes, markets appeared increasingly willing to fade headline risk in the absence of concrete policy follow-through. Consistent with this interpretation, implied volatility remained contained throughout the episode, with the VIX Index briefly spiking only to around 20 before normalising.

Earnings season emerged as a key focal point for investors and a growing source of differentiation. In the United States, around 40-45% of S&P 500 companies had reported by month-end, with roughly three quarters beating earnings expectations and around 60% exceeding revenue forecasts. In Europe, reporting progress was slower, with roughly 30% of Euro Stoxx 50 constituents having published results and earnings beats closer to the mid-50% range, consistent with weaker cyclical momentum. While aggregate earnings growth remains supportive, guidance and margin commentary have become more influential in shaping market reactions, particularly within the Tech sector.

This shift was most clearly illustrated by weaker-than-expected results from Microsoft, which became a pivotal moment for the AI narrative. While demand for AI-related products and services remains strong, Microsoftˇs earnings highlighted the rising capital intensity of AI infrastructure build-out and a slower pace of near-term monetisation. The market response underscored growing sensitivity to execution risk, return on invested capital and margin sustainability across the AI complex. Importantly, this has not marked an end to the AI theme, but rather a rotation within it. Investor focus has increasingly shifted toward specific bottlenecks in the supply chain, most notably the memory segment, where high-bandwidth memory is emerging as a critical constraint for AI deployment. This rotation drove outsized gains in several memory-related semiconductor stocks (e.g. Sandisk, Micron, Western Digital) during January and reinforced a broader trend toward higher single-stock volatility and dispersion within technology indices.

Macro data in the U.S. softened modestly but did not signal a material deterioration in growth. Labour-market indicators continued to cool gradually, while services inflation remained sticky, reinforcing the view that the economy is decelerating toward trend rather than tipping into recession. Monetary-policy expectations stabilised over the month, with markets continuing to price a limited easing cycle later in 2026. Communication from the Federal Reserve remained cautious and data-dependent, emphasising the need to avoid prematurely loosening financial conditions. Against this backdrop, the nomination of Kevin Warsh briefly drew market attention, reinforcing investor focus on central-bank credibility, balance-sheet discipline and the longer-term implications for real rates, even if no immediate policy shift is implied. Warshˇs nomination was broadly well received, with markets taking comfort in his credibility and policy experience, and early concerns around a more overtly politicised appointment fading quickly. Having said that, Warsh is also widely perceived as more hawkish than the marketˇs median expectation, particularly on inflation credibility, balance-sheet discipline, and tolerance for prolonged restrictive policy.

In fixed income, government bond yields remained elevated but range-bound. U.S. Treasury yields drifted slightly higher at the long end, reflecting persistent term premia, heavy issuance and concerns around fiscal sustainability, while front-end rates were anchored by expectations of a gradual and limited easing cycle from the Federal Reserve. This kept real yields restrictive and continued to act as a headwind for duration-sensitive assets. Overall, Credit markets remained constructive, with spreads near cycle tights, but showed early signs of fatigue. While default rates remain low, investors are increasingly discriminating, particularly in lower-quality and private credit segments, where tight spreads offer limited compensation for refinancing risk in a higher-for-longer rate environment.

The U.S. dollar continued the 2025 trend and softened modestly against major peers, reflecting easing growth momentum, stabilising expectations around rate cuts later in 2026, and persistent concerns over fiscal deficits and heavy Treasury issuance.

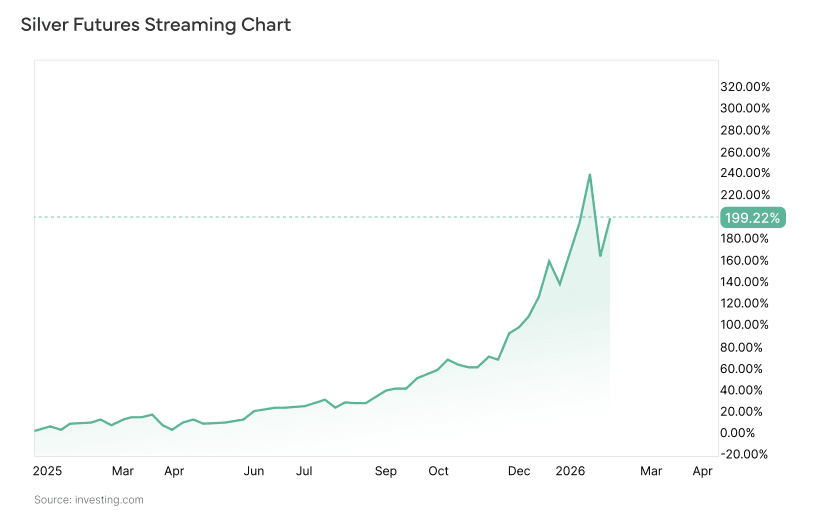

Precious metals experienced a sharp positioning-driven shock late in the month. On Friday, 30 January, gold and silver sold off aggressively amid forced deleveraging by leveraged retail and momentum-oriented investors. Gold experienced its steepest daily decline since the early 1980s dropping around 9% intraday from record highs bringing prices down from just under all-time peaks toward the mid-$4,000/oz range. Silverˇs sell-off was even more dramatic, with prices plunging around 31% in a single session, marking one of the most severe one-day declines in decades for the white metal. The move was exacerbated when CME Group raised margin requirements on gold and silver futures in response to the steep price declines. The margin changes amplified cross-asset deleveraging, with spillovers into equities and other risk assets during the same session. Importantly, the sell-off in precious metals appeared technical rather than fundamental, with central-bank demand, a weaker U.S dollar, geopolitical hedging needs and longer-term fiscal concerns remaining intact.

Following the early-January geopolitical shock surrounding the US military intervention in Venezuela, oil prices initially showed some volatility but ultimately remained anchored within familiar ranges. In the days after the event, oil futures saw modest upticks as markets weighed potential supply implications, though the moves were limited and short-lived given abundant global supply and the fact that Venezuelan exports remain a small share of total crude flows. Markets largely concluded that any meaningful increase in Venezuelan production would require substantial investment and time, leaving near-term oil price dynamics driven more by broader demand trends and OPEC+ actions than by the political episode itself.

Overall, January reinforced a classic late-cycle macro environment. Growth remains resilient but less forgiving, liquidity is no longer expanding aggressively, and asset-price performance is increasingly driven by earnings quality, capital discipline and balance-sheet strength rather than broad multiple expansion.

Digital asset markets entered January attempting to stabilise after the volatility of late 2025, but the month ultimately reinforced cryptoˇs sensitivity to macro conditions, liquidity, and market structure. Supported by renewed acquisitions from MicroStrategy, Bitcoin rallied to around $97k mid-month, briefly reclaiming the $90 92k resistance zone. Momentum, however, proved short-lived, fading amid regulatory uncertainty, mixed macro signals and adverse market flows. By month-end, BTC had slipped back toward the low-$80k area, leaving the market on fragile footing heading into the final weekend.

That fragility was exposed during the final days of the month. Over Saturday 31 January, Bitcoin fell by roughly 6.5% to around $78.7k, while Ethereum underperformed, declining by approximately 11.8% to ~$2.39k. The move extended into Sunday, with BTC briefly trading below $77k in thin weekend liquidity, marking one of its sharpest short-term drawdowns in several months. The sell-off was broad-based rather than confined to majors, with large-cap crypto benchmarks down around 10% on a 7-day basis around month-end, consistent with a market-wide deleveraging episode. Liquidations were material, with estimates pointing to roughly $2bn of forced unwinds as prices accelerated lower, underscoring that leverage and positioning rather than a single fundamental catalyst drove the speed of the move. Perpetual funding rates turned decisively negative into month-end, particularly for ETH and high-beta altcoins, reflecting defensive positioning and short-side demand for protection. It is also worthwhile highlighting that negative funding did not immediately stabilise prices, highlighting that funding signals were overwhelmed by liquidity-driven flows rather than mean-reversion dynamics.

Importantly, the late-January sell-off was not crypto-specific in origin. Digital assets traded macro-first into month-end, with weakness coinciding with broader cross-asset deleveraging and a deterioration in risk appetite, most notably in precious metals (see above). The downside in BTC and ETH appears closely linked to tighter liquidity conditions and shifting policy expectations, reinforcing cryptoˇs current behaviour as a high-beta expression of global risk sentiment during periods of stress. Market structure then amplified the move: weekend liquidity conditions proved decisive, with thinner order books and reduced arbitrage capacity leading to wider cross-venue price dispersion and greater price impact from forced selling.

As in prior episodes, timing mattered as much as magnitude, with pressure that may have resulted in a more orderly repricing during weekday hours instead translating into a sharp, nonlinear move under weekend conditions. Overall, Bitcoin closed the month down -10%, while ETH posted losses of -18%. Altcoins materially underperformed BTC, with many large-cap alts down 15 25% over the final two weeks of January, reflecting a broad reduction in risk tolerance rather than idiosyncratic protocol issues.((Spot Bitcoin ETFs experienced renewed outflows late in the month, coinciding with the break below $80k. Daily outflows peaked at close to $800m on 29 January, signalling short-term institutional de-risking rather than steady accumulation. The procyclical nature of ETF flows reinforced the view that regulated vehicles are currently amplifying, rather than dampening, spot market moves during periods of stress.

On the DeFi side, it is important to note that similar to the October 10 events DeFi liquidation mechanisms remained orderly during the late-January sell-off, with no major oracle failures or protocol-level stress reported. However, CeFi venues continued to dominate liquidation volume, reinforcing the view that leverage and cross-margin structures remain the primary transmission channel for systemic stress in crypto markets. Aggregate stablecoin supply was broadly flat in January, with no meaningful expansion to offset declining risk appetite. USDT issuance slowed, while USDC saw mild net redemptions. On-chain transaction volumes declined across major L1s, consistent with reduced speculative activity rather than stress-driven flight from centralised venues.

Option markets also reflected the transition from complacency to stress as well. Implied volatility remained compressed for much of January but repriced sharply higher at the front end into month-end as spot prices broke key levels. The Deribit Dvol index traded at its highest point since early December. The Volatility term structure briefly inverted, with front-end implied volatility exceeding longer-dated tenors - a classic sign of near-term stress rather than long-term repricing. Options skew turned more defensive, with puts trading at a significant premium to calls across parts of the surface during the sell-off, before partially normalising as conditions stabilised. At the same time, overall derivatives positioning remained cleaner than in prior cycles but nonetheless defensive. BTC options open interest had already declined materially from its October 2025 peak of roughly $57bn to around $28bn by January, reflecting a broader de-grossing of risk following last yearˇs highs. While this reduced the likelihood of extreme liquidation cascades, it also left the market more sensitive to incremental flows and short-term positioning effects, particularly around major expiries where strike concentrations continued to influence spot behaviour.

Against this backdrop, regulation remained an important but unresolved theme. In the U.S., the Digital Asset Market CLARITY Act and related market-structure efforts continued to feature prominently in policy discussions, though progress remains uneven and the legislative path uncertain. Incremental guidance from the SEC around broker-dealer custody and trading of digital assets on regulated venues has provided marginal clarity, but has not yet altered the broader regulatory regime. In Europe, attention has shifted decisively from legislation to implementation, with MiCA moving into an operational phase focused on licensing, supervision and enforcement. The UK, meanwhile, has maintained a cautious stance on retail access and platform compliance, keeping distribution and marketing constraints firmly in focus.

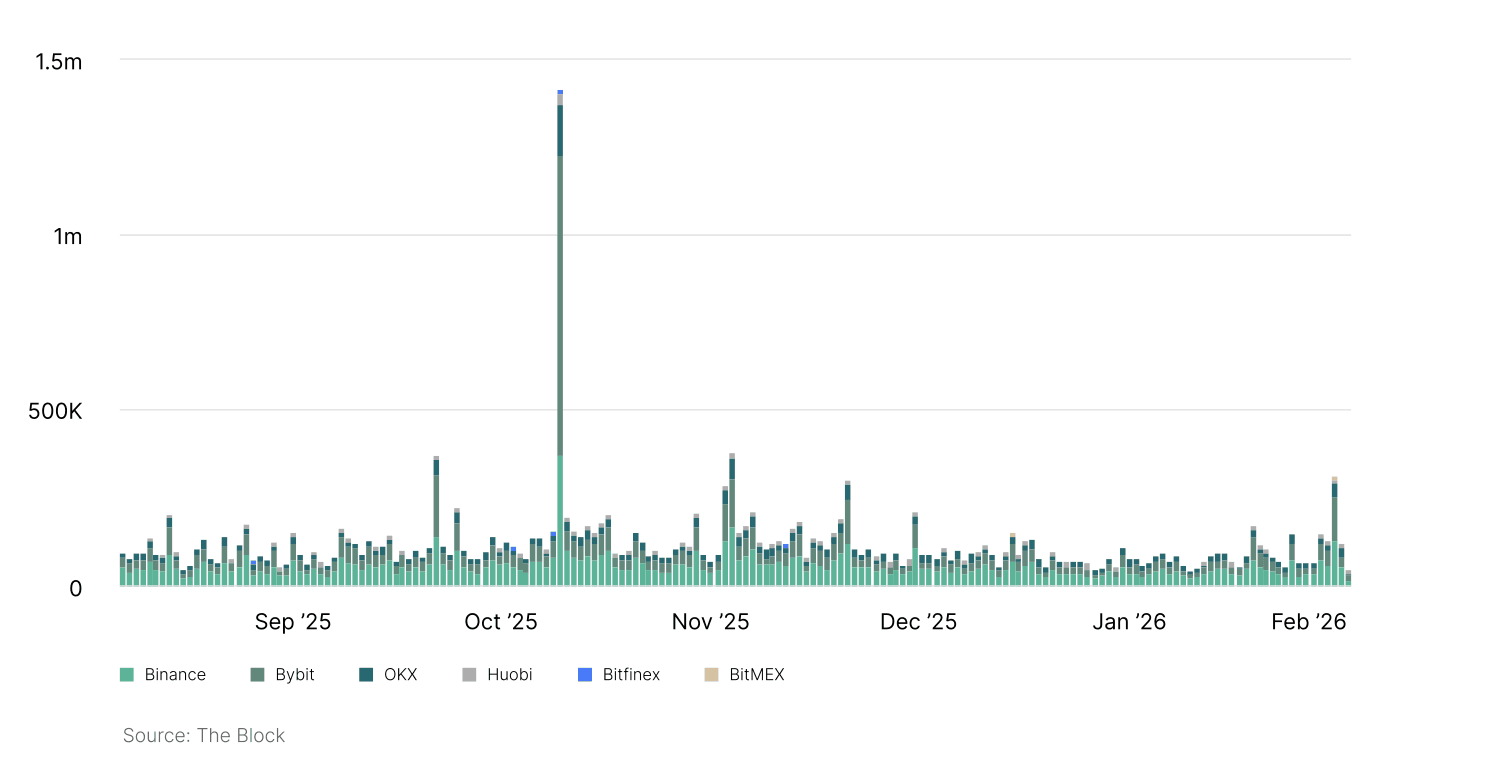

The daily volume of liquidations on futures exchanges increased on 31 January, but remained well below the levels observed during the October 10 liquidation event.

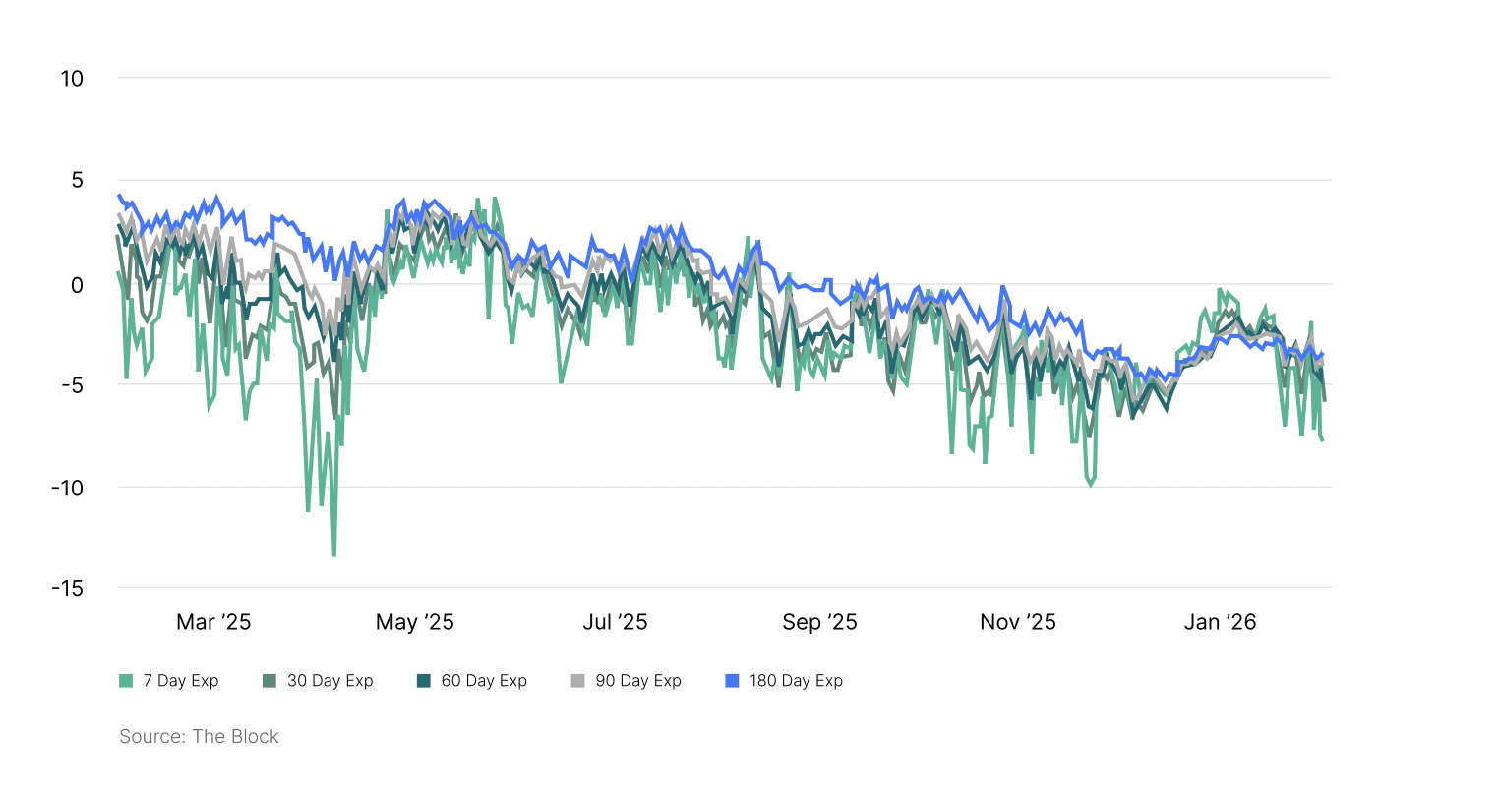

The 25-day option skew remained in a clear downtrend throughout January, signalling a persistent preference for puts over calls across all maturities. While skew briefly improved early in the month, the subsequent spot sell-off pushed it back toward its prevailing downtrend by month-end.

Overall, January illustrated a digital-asset market caught between improving internal structure and deteriorating liquidity conditions. Leverage has normalised, derivatives positioning has reset, and excesses seen in prior cycles have been reduced. At the same time, thinner liquidity, heightened macro sensitivity and unresolved regulatory questions have made prices more vulnerable to sharp, technically driven moves. The late-January sell-off served as a clear reminder that, in the current regime, market structure, liquidity and overall sentiment - rather than the crypto specific narrative alone remain the dominant drivers of short-term price dynamics, even as the longer-term investment case continues to hinge on regulation, institutional adoption and capital flows.

Disclaimer:

Investment advisory and asset management services are provided by Lionsoul Global Advisors LLC (˝Lionsoul Global Advisors˛), an investment adviser registered with the Texas State Securities Board (CRD #: 324883). Information presented, displayed, or otherwise provided is for educational purposes only and should not be construed as investment, legal, or tax advice, or an offer to sell or a solicitation of an offer to buy any interests in a fund or other investment product. Access to the products and services of Lionsoul Global Advisors is subject to eligibility requirements and the definitive terms of documents between potential clients and Lionsoul Global Advisors, as they may be amended from time to time.

Past performance is not indicative of future results, and there can be no assurance that the portfolio will achieve its investment objectives or that any investment strategy will be successful.

Certain statements contained herein constitute forward-looking statements, including statements regarding anticipated market conditions, portfolio positioning, and expected opportunity sets. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied. Forward-looking statements speak only as of the date made and are subject to change without notice.