Insights

Digital Asset Market - Feb in Review

Insights

Digital Asset Market - Feb in Review

February underscored that markets are currently as sensitive to positioning and narrative as they are to fundamentals. Headline indices were deceptive: beneath them, dispersion increased sharply, particularly within U.S. technology, where volatility rose, and sector leadership fractured. The divergence between a resilient Dow and a weaker Nasdaq reflected a meaningful shift in investor behaviour– capital rotated away from names exposed to AI disruption risk, as participants grew increasingly sceptical of the durability of traditional software business models and responded with outsized force to incremental news flow. At the same time, digital assets experienced a structurally significant but mechanically driven dislocation early in the month. This episode illustrates how derivatives positioning, ETF flows and liquidity dynamics can amplify moves far beyond fundamental catalysts. Importantly, the sell-off did not occurring isolation. Digital assets became increasingly entangled with the broader Nasdaq-driven risk-off dynamic, with the correlation between Bitcoin and U.S. technology equities rising meaningfully during stress windows. As tech volatility increased and systematic deleveraging accelerated, Bitcoin traded less as an idiosyncratic asset and more as a high-beta extension of the growth complex, reinforcing cross-asset feedback loops. While macro conditions remained broadly stable, both traditional and digital markets displayed heightened fragility – an environment in which sentiment shocks and positioning imbalances can outweigh earnings revisions or policy surprises. Late in the month and into early March, markets also began to price the risk of geopolitical escalation in the Middle East following joint U.S.–Israeli strikes on Iran and subsequent retaliation, raising concerns about potential disruption through the Strait of Hormuz, a chokepoint for roughly 20% of global seaborne oil flows. Oil prices initially spiked by more than 10% toward the $80–82 per barrel range, while global equities weakened and safe-haven assets such as gold saw renewed inflows as regional risk premia rose. Although some of the initial moves later partially retraced as investors reassessed the likelihood of sustained disruption, the episode underscored how quickly energy market shocks can transmit into broader equity and commodity volatility. Overall, February did not mark a deterioration in economic fundamentals. Rather, it exposed a regime in which markets are quicker to price downside scenarios, quicker to amplify technical flows, and less tolerant of ambiguity.

February was characterised less by broad index-level weakness and more by rising internal dispersion and elevated single-stock volatility, particularly within U.S. technology and software. While headline indices suggested relative stability, underlying price action revealed a market increasingly sensitive to narrative shifts and positioning. For the month, the S&P 500 declined by approximately 0.9%, the Nasdaq Composite fell 3.4%, and the Dow Jones Industrial Average gained 0.2%. The divergence between indices was notable. The Dow reached fresh intra-month highs, surpassing the 50k mark for the first time, while the Nasdaq experienced a pronounced drawdown, highlighting a clear rotation away from growth-duration exposure and toward more defensive and cyclically anchored names. U.S. software stocks were at the epicentre of the volatility. Importantly, the weakness was not driven by a collapse in earnings, but by a narrative that rapid advances in artificial intelligence could structurally compress pricing power in traditional software models. The argument, increasingly discussed across markets, suggests that the cost of developing customised software may fall exponentially as AI capabilities improve, potentially challenging the long-term economics of incumbent providers. Whether or not such disruption materialises in the near term, the mere plausibility of the theme was sufficient to trigger de-risking in a market that was already fragile.

Dispersion trades gained popularity during the month, with single-name volatility in technology rising relative to the broader S&P 500. Index-level hedging gave way to stock-specific positioning, amplifying moves beneath the surface. Even strong corporate results were insufficient to restore confidence. Nvidia’s earnings, while fundamentally solid, were accompanied by guidance perceived as less optimistic than prior quarters. In a jittery tape, good results were no longer enough; the reaction function had clearly shifted.

More broadly, the market appeared increasingly predisposed to sell first and analyse later. Viral “doomsday” research pieces such as the one by Citrini Research and speculative disruption narratives, which might have been ignored in a more constructive environment, gained traction and contributed to momentum-driven weakness. For example:

Shares of U.S. logistics companies sold off sharply after Algorhythm Holdings, a micro-cap company that recently pivoted from selling karaoke machines to AI-driven logistics tools, announced a product aimed at improving trucking efficiency. Despite its roughly $6 million market cap, the announcement triggered heavy losses in established freight names such as RXO (–20%) and C.H. Robinson (–14%), wiping out tens of billions in market value. That a karaoke vendor could reshape sentiment across an entire sector said less about the news itself than about the environment receiving it. In isolation, these inputs were unlikely to justify the scale of market moves. In aggregate, however, they reinforced a sentiment regime characterised by heightened sensitivity and limited tolerance for ambiguity.

Yields remained elevated but broadly range-bound, reinforcing the higher-for-longer narrative without triggering a disorderly repricing. The nomination of Kevin Warsh as chair of the U.S. Federal Reserve – continued to attract attention. While initially interpreted as hawkish, Warsh has previously emphasised that structural productivity gains, including those driven by technological innovation, are disinflationary overtime. If taken at face value, this framework implies lower equilibrium yields in the medium term, suggesting that recent fears of sustained policy tightening may be overstated.

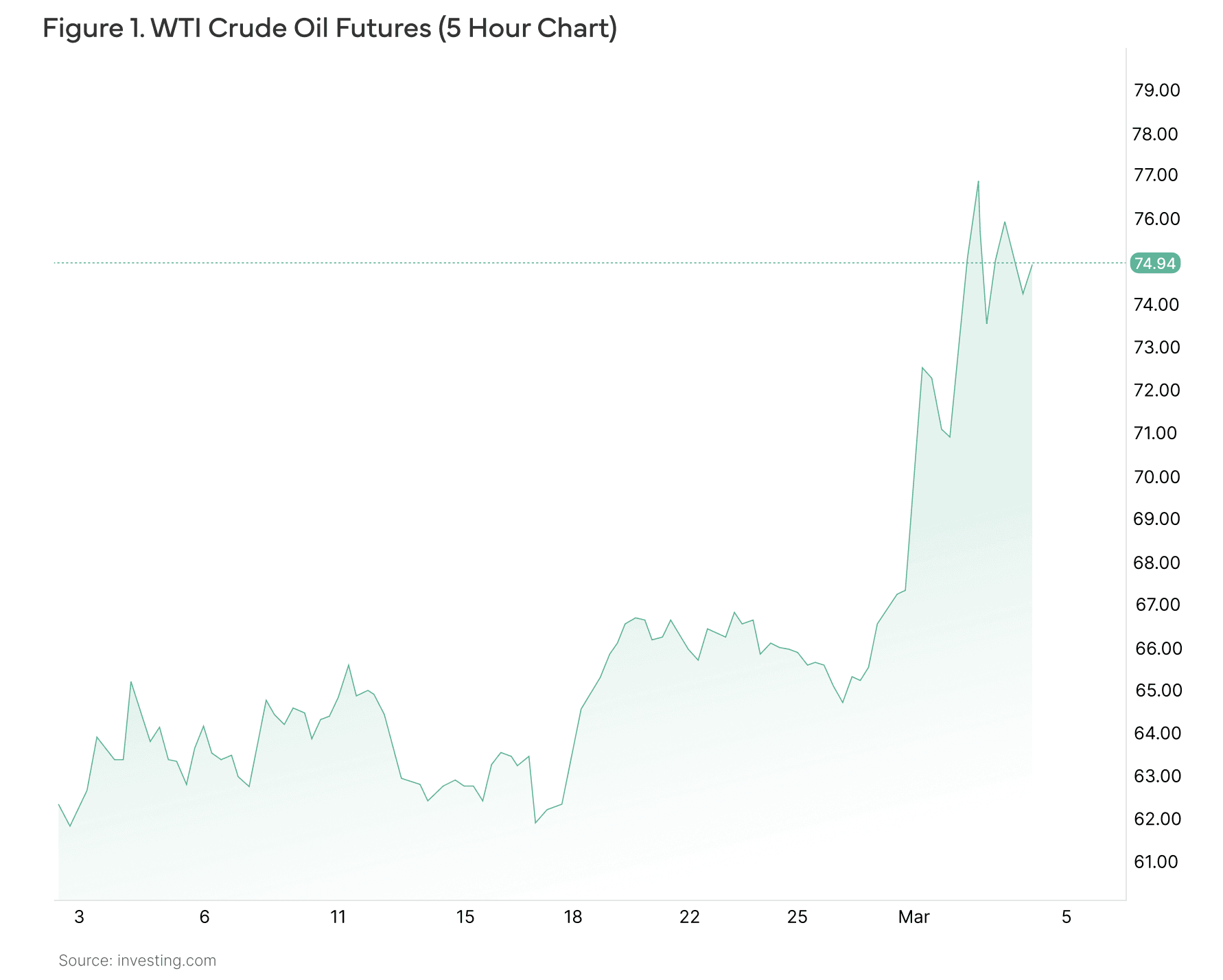

Late in the month and into early March, escalating tensions involving Iran reintroduced geopolitical risk premia into global markets. Oil prices moved sharply higher amid concerns overpotential disruptions to shipping through the Strait of Hormuz, while equity futures weakened on escalation headlines. Gold also rallied as investors sought traditional safe-haven assets.

The escalation in Iran took markets by complete surprise. Oil jumped by approximately 15% in the immediate aftermath, increasing the risk of further shocks to global supply chains and renewed inflationary pressures.

Digital assets remained tightly linked to broader risk sentiment throughout February. Bitcoin briefly traded near$60,000 during the early-February deleveraging episode before recovering toward the $70,000 area as broader markets stabilised. Importantly, BTC continued to hold above or near its 200-day moving average, a level that has historically acted as medium-term support during corrective phases within structurally constructive regimes.

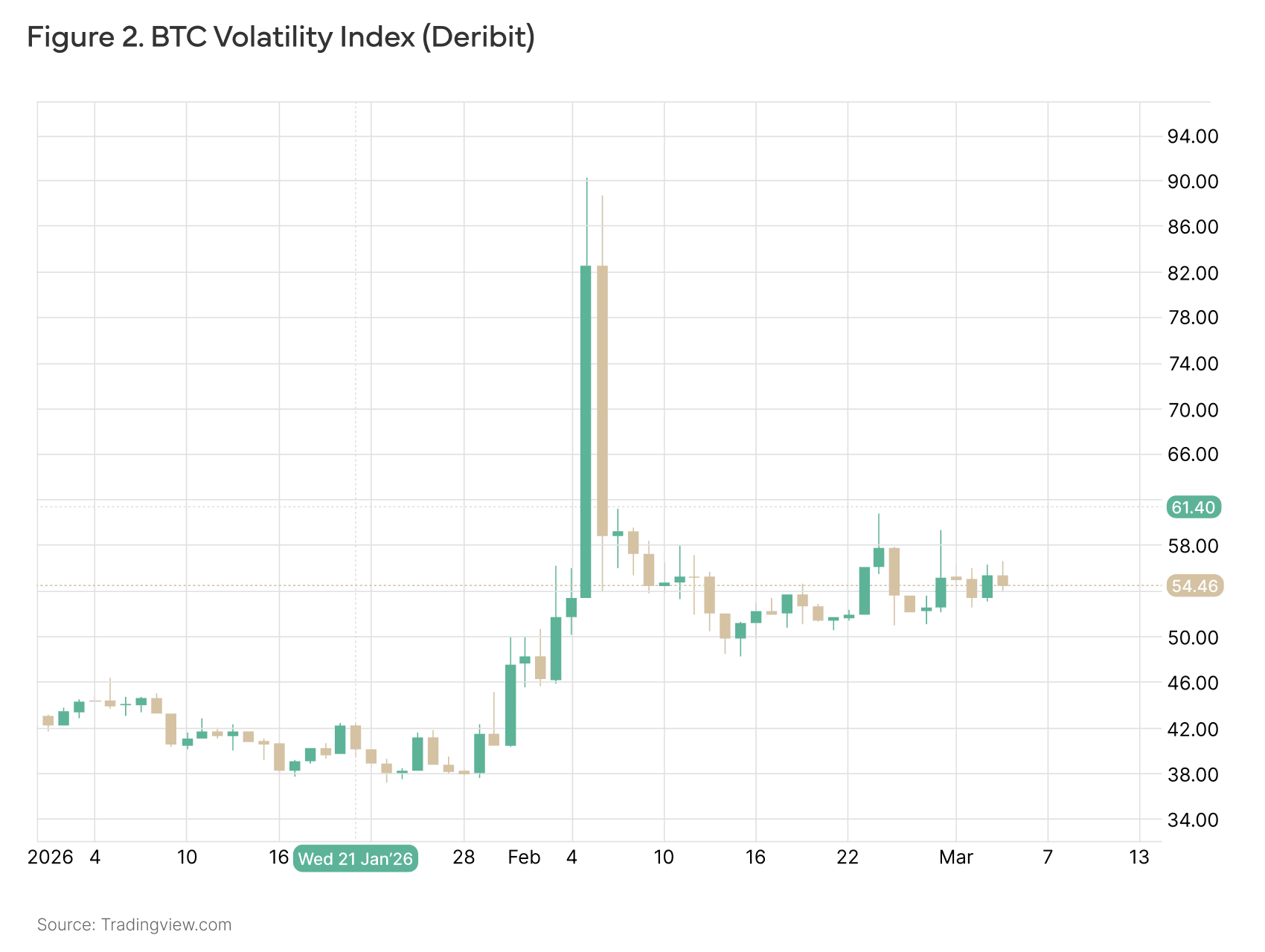

The most significant crypto-specific development occurred during the 5–6 February sell-off, which appeared driven more by cross-asset de-risking and market structure dynamics than by crypto-native catalysts. The magnitude of the move was exceptional. On February 5, Bitcoin fell from approximately $70,700 to $60,000 within a matter of hours – a 15% decline, comparable in extremity to the March 2020 COVID crash. At the same time, the Deribit Volatility Index (DVOL) surged from roughly 55 to 90 within six hours, a 64% implied volatility shock. It looks like the move was largely triggered by rapid de-grossing across multi-strategy and macro funds. Evidence suggests that short-gamma positioning and dealer hedging flows amplified downside pressure as market makers sold into weakness to rebalance exposure. Importantly, ETF flow data did not indicate sustained end-investor capitulation. Bitcoin ETFs recorded net creations rather than redemptions during the dislocation, suggesting that price action was primarily driven by derivatives positioning, dealer hedging, and cross-asset risk reduction within the “paper” market complex rather than structural selling by long-only holders

Derivatives markets reflected continued caution over the month. Funding rates normalised from late-January extremes but remained subdued relative to prior speculative peaks. Ethereum funding briefly turned neutral to negative during stress windows, underscoring limited appetite for leveraged long positioning. Bitcoin options open interest remained materially below October2025 highs, reflecting a cleaner leverage profile and reduced systemic tail risk. Volatility term structure briefly inverted during stress periods before normalising.

Liquidity conditions remained thinner than in late 2025. Trading volumes improved modestly from January lows but continued to operate below prior cycle peaks. Weekend liquidity remained structurally weaker than weekday sessions, preserving the potential for nonlinear price moves during off-peak hours. Stablecoin supply growth remained muted, suggesting limited incremental risk expansion within the ecosystem.

Deribit Dvol index surged from 55 to 90 within 6 hours on February 5th.

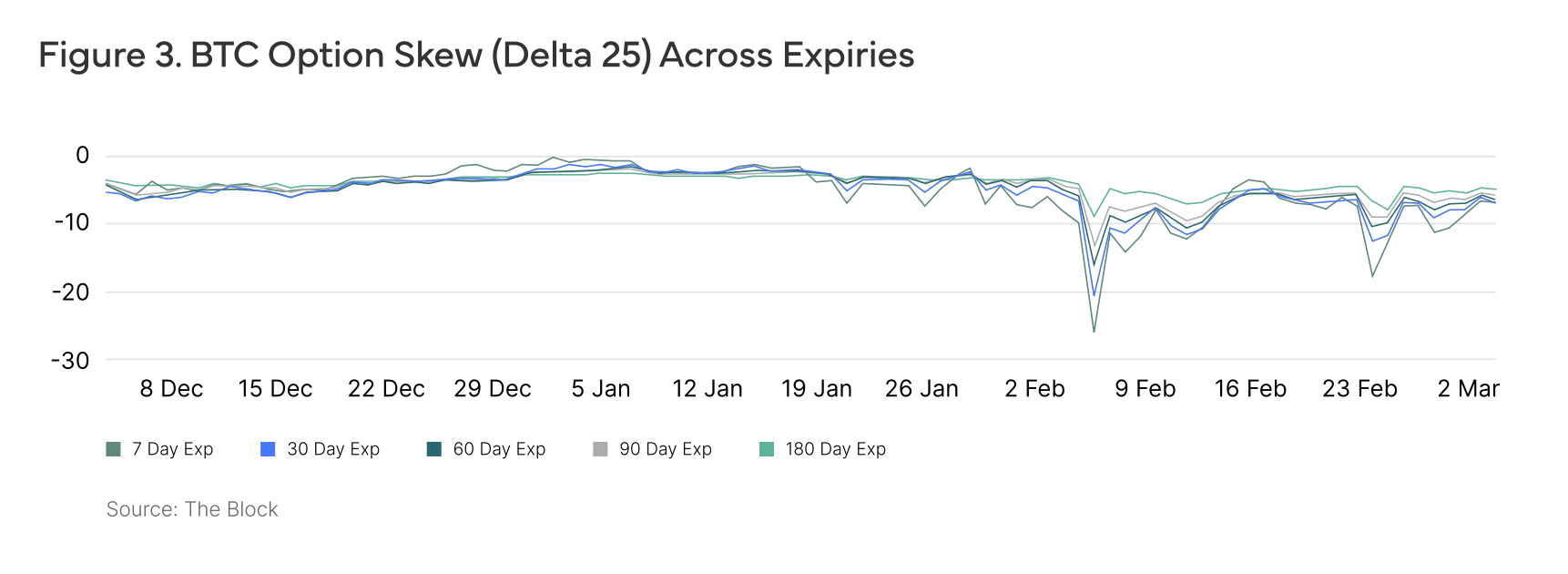

BTC 25-delta option skew has been trading in negative territory over the past three months and dipped significantly in early February, as comparable puts have become more expensive than calls, indicating overall negative sentiment and positioning in the options market.

Taken together, February suggests that markets are operating in a regime defined by higher dispersion and greater sensitivity to positioning, but not by structural deterioration. In digital assets in particular, the early-month dislocation appears to have flushed leverage from the system, leaving positioning materially cleaner than in prior peaks. Funding rates remain subdued, open interests well below late-2025 highs, and sentiment indicators reflect caution rather than excess.

Technically, price action is beginning to look more consistent with consolidation than acceleration. After several consecutive weeks of pressure, Bitcoin has stabilised and is trading within a narrowing range, a pattern often associated with markets transitioning from trend to base-building. Correlated growth assets, particularly within U.S. technology, are displaying similar signs of exhaustion, reinforcing the idea that downside momentum may be moderating rather than intensifying.

Importantly, digital assets did not materially extend losses during the recent Iran-related geopolitical escalation, despite volatility in oil and equities. This relative resilience, combined with cleaner positioning and more defensive sentiment, suggests that systemic fragility has diminished. While volatility and narrative-driven swings are likely to persist, the current backdrop appears increasingly characterised by consolidation rather than renewed structural deterioration.

Investment advisory and asset management services are provided by Lionsoul Global Advisors LLC (“Lionsoul Global Advisors”), an investment adviser registered with the Texas State Securities Board (CRD #: 324883). Information presented, displayed, or otherwise provided is for educational purposes only and should not be construed as investment, legal, or tax advice, or an offer to sell or a solicitation of an offer to buy any interests in a fund or other investment product. Access to the products and services of Lionsoul Global Advisors is subject to eligibility requirements and the definitive terms of documents between potential clients and Lionsoul Global Advisors, as they may be amended from time to time.

Past performance is not indicative of future results, and there can be no assurance that the portfolio will achieve its investment objectives or that any investment strategy will be successful. Certain statements contained herein constitute forward-looking statements, including statements regarding anticipated market conditions, portfolio positioning, and expected opportunity sets. Such statements involve known and unknown risks, uncertainties, and other factors that may cause actual results to differ materially from those expressed or implied. Forward-looking statements speak only as of the date made and are subject to change without notice.