Reports

Digital Asset Market - October in Review

Reports

Digital Asset Market - October in Review

October delivered one of the more paradoxical months of the year — a period marked by renewed tariff tensions, an unprecedented liquidation in digital assets, and yet a strong rebound and continued strength across traditional markets. Despite a string of disruptive headlines, risk appetite proved remarkably resilient. Equity markets on both sides of the Atlantic extended their rally to fresh all-time highs, volatility quickly subsided, and credit spreads tightened to multi-year lows. What might have been a turning point instead reinforced the prevailing late-cycle narrative: investors are willing to look through near-term disruptions in the belief that policy easing and structural growth in AI will keep the cycle alive.

Meanwhile, digital-asset markets experienced one of the most violent dislocations in their history. Triggered by the same U.S.–China tariff shock that equities quickly digested, over-leveraged crypto markets suffered a cascading liquidation that erased more than US $500 billion in market value within hours. Within a single day, more than $19 billion in leveraged positions (mostly long perpetual futures) were wiped out — the largest 24-hour liquidation event ever recorded in crypto markets. 1.6 million trader accounts were affected. The scale of forced unwinds revealed structural weaknesses in centralised-exchange risk engines and the fragility of cross-margin systems. Yet, DeFi protocols emerged as relative winners, underscoring the maturing architecture of decentralised markets.

While the scale of forced unwinds is likely to reveal additional casualties among leveraged hedge funds, market makers, and lending platforms over the coming weeks and months, the episode may ultimately act as a catharsis for the ecosystem. The crisis has refocused attention on venue risk, margin architecture, and collateral quality — areas long overshadowed by the chase for yield and returns. With speculative leverage largely flushed out, liquidity provision more selective, and fewer participants competing for short-term alpha, the market may now enter a healthier, more sustainable phase. In many ways, this reset could pave the way for more disciplined institutional engagement, greater focus on operational resilience, and a more transparent separation between exchange risk and asset-level fundamentals.

Taken together, October illustrated both sides of the current investment climate: resilience driven by liquidity, innovation, and policy support — and fragility born from leverage, valuation excess, and hidden interconnections. As we move into year-end, the challenge for investors is to distinguish between cyclical noise and structural change — and to remain positioned for opportunity without losing sight of risk discipline.

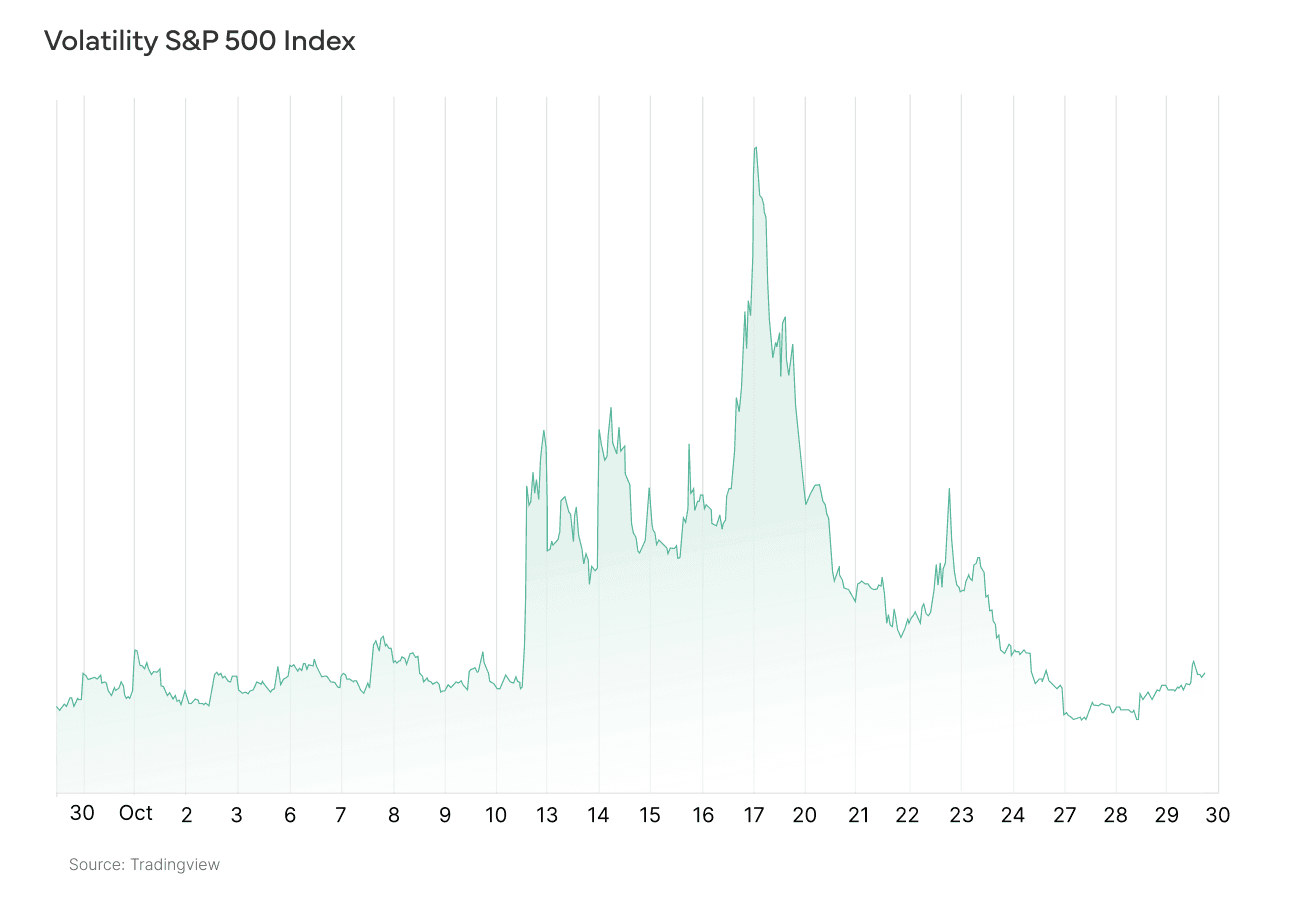

October extended the positive momentum of recent months, with most major indices on both sides of the Atlantic hitting new all-time highs. Beyond the headline numbers, however, it was a bumpy ride as President Trump announced new tariffs of 100% on Chinese goods on October 10 in reaction to China’s rare-earth export controls. The announcement triggered a brief risk-off move: the VIX spiked to around 25, and the S&P 500 and Nasdaq fell sharply on the news. However, as so often is the case, the panic was short-lived as the so-called TACO trade (“Trump Always Chickens Out”) once again came into play.

By the end of the month, the proposed tariffs were effectively off the table amid signs of a potential deal in which China would soften its planned restrictions on rare-earth minerals. Tail-risks to global supply chains have therefore eased materially since the initial headlines. As a sign of renewed risk-on sentiment, the VIX retraced to 16 — below its longer-term average.

At the same time, gold also pulled back modestly from its recent all-time highs. However, part of the drawdown appears to reflect a healthy technical correction rather than a shift in sentiment. The metal remains attractive as a macro hedge against USD weakness, central-bank policy uncertainty, sticky inflation, and record-high equity valuations.

Equity markets ended the month firmly higher, with the S&P 500 up roughly 2.3%, the Nasdaq 4.8%, and the Euro Stoxx 50 around 2.4%. Bond yields edged lower on moderating inflation data and rising expectations of Fed rate cuts in early 2026, reinforcing a broadly supportive backdrop for risk assets.

While the U.S. government shutdown has delayed key data releases and clouded the outlook for policymakers, encouraging September inflation data shifted expectations toward the Federal Reserve continuing its easing cycle, cutting rates by 25 basis points and ending its quantitative tightening campaign. The move, however, should not mask the fact that the Fed remains in a delicate position: inflation is still somewhat above target, while the economy shows signs of fragility, with labour-market softening, persistent tariff pressures, and trade-related cost stickiness. Due to the limited availability of recent government data, the Fed noted that its visibility remains impaired, prompting a more cautious stance on future rate cuts, including the potential move in December.

On a positive note, U.S. corporate earnings have once again surprised to the upside. Analysts have now upgraded their expectations to around 10.4% year-on-year earnings growth for S&P 500 companies. This would mark the strongest quarterly performance in nearly two years.

Across the Atlantic, the earnings picture remains more muted. Pan-European indices such as the STOXX 600 are expected to post roughly flat earnings growth, although Eurozone blue chips — particularly in banking, luxury, and industrial-export sectors — have performed well in October. The rally appears to be supported by a softer euro, growing expectations of ECB rate cuts, and easing concerns over global trade tensions.

In the U.S., the breadth of the rally has continued to expand as sectors such as industrials, materials, and even autos have started to participate. However, it remains primarily technology and AI-infrastructure names — notably semiconductors and cloud-computing firms — that dominated the October advance. Nvidia made history by becoming the first company to reach a US $5 trillion market capitalisation, underscoring investor enthusiasm for AI. The bullish narrative is underpinned by its dominant position in AI infrastructure, particularly GPUs used for training large language models.

Alongside that optimism, however, concerns over valuation excess are growing. In a rather controversial development, OpenAI has entered a network of large-scale partnership deals with infrastructure providers including Nvidia, AMD, Oracle, and Broadcom. These agreements have drawn attention for creating what market observers call a “circular trade” — a loop of capital, hardware sales, and strategic investments in which hardware vendors lend or invest capital in their customers (or partners) with the expectation that those customers will use the funding to purchase additional hardware from the same vendors. In effect, the vendor fronts capital for infrastructure build-out that generates further hardware sales back to itself, creating a self-reinforcing demand cycle.

The risk with such trades is that they can become self-fulfilling rather than organically driven, raising the prospect of overcommitment, potential supply gluts, margin compression, and valuation overshoot. Some commentators view this dynamic as a built-in tail risk, reminiscent of patterns seen in the late-1990s dot-com bubble. According to the Financial Times, OpenAI’s cumulative computing-power commitments — across deals with Nvidia, AMD, Oracle, and others — now exceed US $1 trillion over the coming decade. These commitments, which vastly outstrip OpenAI’s current revenues, imply extraordinary growth expectations and leave little margin for disappointment if AI adoption or monetisation falls short of projections.

On the credit side, the bankruptcy of auto-parts conglomerate First Brands Group grabbed headlines. In its Chapter 11 filings, the company listed liabilities of roughly US $9 billion in known debt, though some estimates place total obligations as high as US $10–50 billion, against a much smaller asset base of US $1–10 billion. The collapse exposed extensive use of opaque, off-balance-sheet financing structures — including receivables factoring, supply-chain and inventory financing, and in some cases the alleged “double-pledging” of invoices. Major creditors and investors, including UBS and Jefferies, now face material exposure. While First Brands may ultimately prove to be an isolated case, its failure has reignited concerns about eroding lending standards and potential contagion across banks, private-credit funds, and trade-finance vehicles. The episode comes at a time when private-credit issuance has surged and U.S. corporate credit spreads are hovering near multi- year lows, underscoring late-cycle complacency.

In such an environment, weaker credits are more likely to surface, particularly if the macro backdrop deteriorates or rates remain elevated. First Brands may therefore represent not just a one-off default, but an early indicator of latent stress building within the private-credit ecosystem.

The VIX Index spiked following the announcement of new China tariffs but quickly reverted to its historical lows, indicating that risk-on sentiment has swiftly returned across equity markets.

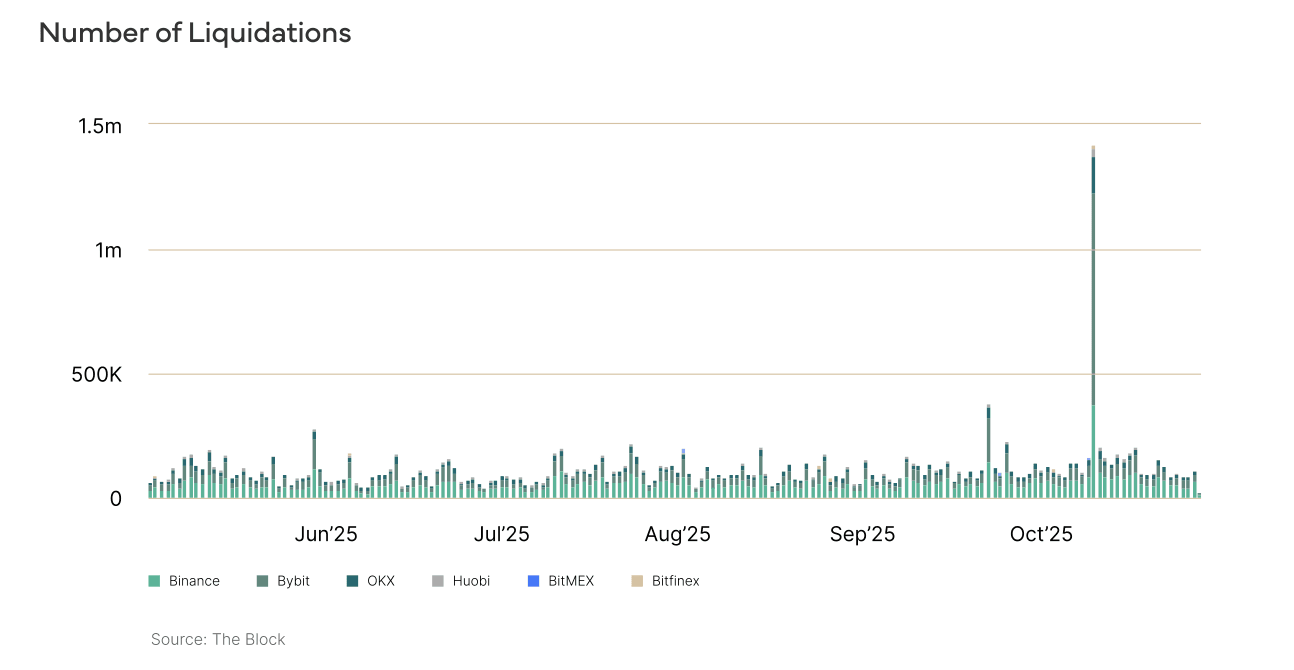

October, a seasonally strong month for digital assets, started off with an uptick across digital assets with Bitcoin reaching fresh all-time highs above USD 125k and ETH reaching highs of USD 4.3k. However, on October 10, an announcement from the US president to impose a 100% tariff on Chinese imports, accompanied by US export restrictions, reverberated through global markets with risk assets selling off sharply across the board. Digital assets bore the brunt of the shock. Total crypto market capitalisation plunged from $4.3 trillion to $3.7 trillion, erasing roughly $560 billion in a single day. The magnitude of forced liquidations dwarfed previous stress events — including the COVID crash in 2020 and the FTX collapse in 2022, when “only” $1.2 billion and $1.6 billion were liquidated, respectively. At one point, over $7 billion in positions vanished within an hour of the US President’s post on Truth Social. The magnitude of the liquidations were roughly 9x larger than typical “bad days” in previous cycles.

While the immediate catalyst was clearly Trump’s China-focused tariff announcement, it is worth examining the internal market dynamics that amplified the move into a historic liquidation cascade. Several factors contributed to the severity of the event: excessive leverage across major venues, widespread use of cross-margined collateral, and fragmented liquidity conditions. Together, these elements obscured the system’s aggregate exposure and allowed risks to compound in ways that few participants fully appreciated.

Before Trump’s tariff announcement, Bitcoin traded close to its all-time highs and overall sentiment across the digital asset ecosystem was broadly positive. This optimism led to a build-up of excessively leveraged long positions. When the tariff headline broke, Bitcoin fell by 10–12% within minutes, while Ethereum dropped around 13%. Altcoins suffered even more severe losses, with tier-one protocols such as Solana falling by up to 40% on some venues.

While this initial leg down set the stage, it should not, on its own, have caused a once-in-history liquidation event. What followed was a story about market structure.

As digital assets started falling, margin calls were triggered and liquidation engines began dumping large positions into order books that were rapidly vanishing. Market makers widened spreads or withdrew entirely in response to the surge in volatility and infrastructure stress. Depth evaporated just as forced selling was at its heaviest. As prices dropped further, over- leveraged long positions hit maintenance margin thresholds and were liquidated, driving prices down even more and triggering additional liquidations. This cascading margin-call spiral created a classic positive feedback loop.

The situation was aggravated by what Coinbase Research described as a surge in systemic leverage since early May, with directional derivative exposure nearly doubling relative to crypto’s total market capitalisation. Open interest across Bitcoin, Ethereum and major altcoin perpetual futures had climbed to record or near-record levels ahead of the October rally. Investors viewed perpetual futures as cheap upside exposure under the “Uptober” narrative after Bitcoin broke through its previous all-time highs, expecting another leg higher.

Venue fragmentation and infrastructure stress added further fuel to the fire. Binance, the largest centralised exchange, experienced extreme price dislocations in several “pegged” or “wrapped” assets. Within minutes of the initial sell-off, Ethena’s USDe—a synthetic stablecoin designed to track the dollar—traded as low as USD 0.65 on Binance, even though its mint/redeem mechanism remained functional and it continued to trade near par elsewhere. Binance’s wrapped staked ETH (wBETH) fell to around USD 430, and its staked SOL product (BNSOL) collapsed to roughly USD 35, 80–90% below fair value.

The root cause was Binance’s risk engine valuing collateral based solely on prices from its internal order book, which had become illiquid once market makers withdrew. It did not incorporate external venue data. Since these pegged assets served as collateral in cross-margin and multi-asset accounts, their under-pricing triggered further margin calls and forced liquidations, even though the assets still had much higher values on other venues. Those forced liquidations sold even more of the distressed collateral into an already broken market, mechanically pushing prices further away from fair value. Because Binance acts as a reference venue for many risk engines and oracles, the mispricing quickly propagated across other centralised and decentralised exchanges.

As the feedback loop intensified, the market’s plumbing began to fail. Exchanges started rate-limiting APIs, throwing execution errors, or freezing certain order types altogether. Market makers and arbitrage desks were unable to hedge or add margin. Some participants reported being “locked out and liquidated,” meaning their positions were force-closed while they were unable to intervene. Passive liquidity dried up precisely when liquidation engines needed it most, amplifying slippage and making each forced sale more violent.

Counterintuitively, not only leveraged long positions were liquidated during the crash. Short positions—often held by delta- neutral arbitrageurs—were also closed out across several major venues despite being on the right side of the trade. The reason lies in a rarely discussed mechanism called Auto-Deleveraging (ADL), designed as a last-resort safeguard to protect exchanges from systemic losses.

Prior to this event, most market participants paid little attention to ADL. Yet its impact became widely known overnight. Perpetual futures, like total-return swaps, are zero-sum instruments: long holders pay short holders when prices fall, and vice versa when prices rise. To keep contract prices aligned with spot, exchanges apply a periodic funding rate. During stress periods, if a leveraged long cannot top up margin, the exchange unwinds the position by selling spot assets to cover the loss, while short holders receive the corresponding gain.

In extreme scenarios like the October event, however, order books can become so skewed that no one is willing to take the other side of these spot trades. Price impact grows so severe that it threatens the venue’s solvency. Tier-one exchanges maintain insurance funds for such cases, but these can quickly be depleted. As a last resort, exchanges may forcibly close short positions starting from their most profitable traders—a process known as Auto-Deleveraging. In effect, the venue socialises part of the loss by haircutting profitable shorts to maintain system integrity.

ADL was triggered on multiple major venues, including Binance, Bybit, and Hyperliquid, during the steepest phase of the sell- off. Their standard liquidation queues were unable to unwind the massive volume of underwater longs without driving prices toward “infinite negative” territory. Liquidity had become so thin that even Bitcoin, typically the most liquid asset in crypto, could not absorb forced selling fast enough without threatening venue solvency.

It is important to note that ADL did not cause the crash—it was a symptom of how dysfunctional liquidity had become. Yet its activation further fuelled market anxiety, as uncertainty about forced reductions led additional market makers to pull liquidity, perpetuating the downward spiral.

The October 10 liquidation cascade will go down as a humbling experience for the digital asset industry. The sheer magnitude of forced liquidations caught the market completely off guard and exposed significant weaknesses in the market’s microstructure. Yet the subsequent rebound — with Bitcoin recovering to around USD 112,000 the following day — demonstrated that underlying buy-side demand remains healthy.

Open interest across perpetuals and futures fell sharply as speculative froth was purged. With leveraged positioning now materially lower, near-term downside convexity has diminished and the market appears in a healthier state. It remains unclear, however, how severely individual market makers, hedge funds, and lending platforms were affected. As is typical in such situations, market participants are keeping their cards close to their chests. The full extent of the damage will likely become evident only over the coming weeks and months, though it is probable that several hedge funds and potentially market makers have been wiped out. This could reduce the number of active arbitrageurs and create opportunities for the remaining players.

For now, liquidity provision across venues has become more conditional. Spreads are wider, visible depth is thinner, and several trading desks have scaled back cross-exchange arbitrage activity due to concerns about execution reliability during stress events. Market participants are also expected to reduce their use of cross-margin setups and favour cleaner, single- asset collateral instead of “wrapped” tokens. This shift will de-risk the system but at the expense of capital efficiency.

Looking ahead, large tier-1 exchanges such as Binance are unlikely to continue relying solely on internal pricing engines. As affected traders prepare lawsuits, some exchanges have proactively announced compensation programmes. Binance, for instance, committed USD 283 million to users impacted by the de-pegging of tokens such as USDe, wBETH, and BNSOL, and subsequently launched a broader USD 400 million “Together Initiative” to cover losses from the crash more generally. Despite these measures, the announced compensations are a drop in the bucket relative to the overall scale of the event.

Other areas of reform are likely to include standardised index and oracle construction to establish transparent definitions of “fair value”, the introduction of independent circuit breakers on collateral pricing, and improvements to ADL stress logic.

During this extreme flash-crash episode, DeFi emerged as a relative winner in its ongoing competition with centralised exchanges. While CeFi venues struggled with technical failures and liquidation bottlenecks, decentralised protocols remained largely stable. The major DeFi platforms recorded significantly fewer liquidations, no systemic API outages, and only minimal pricing discrepancies, thanks to diversified oracle data feeds. They also lack an ADL mechanism, which prevents profitable traders from being force-closed.

The number of liquidations on October 10 dwarfs previous market stress scenarios by a factor of 9x.

From a broader market-structure perspective, the shake-out — as violent as it was — can ultimately be seen as healthy. It will take time to rebuild confidence across the asset class, but the sell-off may serve as a form of catharsis, flushing out excessive leverage and making market participants more aware of tail risks. The swift rebound suggests that the drawdown was driven primarily by a self-reinforcing feedback loop rather than by a fundamental reassessment of digital assets. The underlying value proposition of the asset class remains intact. Spot ETFs showed limited impact, and both implied and realised volatility quickly mean-reverted following the event. Bitcoin continues to trade within roughly 12% of its all-time highs.

While the expectation of an “Uptober” ultimately did not materialise, we believe that digital assets often perform best when positioning is defensive and sentiment subdued. Historically, periods of pessimism have tended to mark the beginning of renewed momentum. Moreover, the fourth quarter has consistently been the strongest for crypto returns, which supports our view that a resumption of the digital asset uptrend may be imminent.

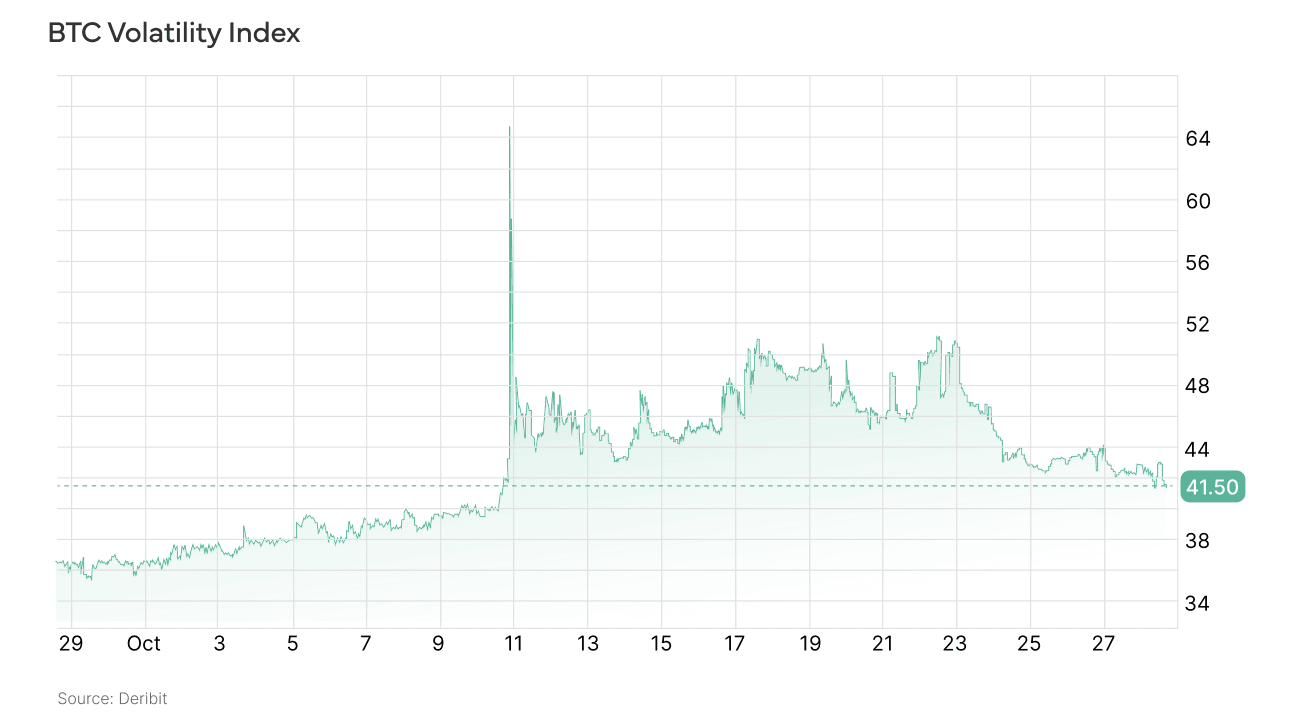

The Deribit Bitcoin DVOL Index — the crypto equivalent of the VIX — spiked sharply during the recent market turmoil but quickly mean-reverted toward its medium-term average. This suggests that the “flash crash” has been largely absorbed by the market.

Disclaimer:

Investment advisory and asset management services are provided by Lionsoul Global Advisors LLC (“Lionsoul Global Advisors”), an investment adviser registered with the Texas State Securities Board (CRD #: 324883). Information presented, displayed, or otherwise provided is for educational purposes only and should not be construed as investment, legal, or tax advice, or an offer to sell or a solicitation of an offer to buy any interests in a fund or other investment product. Access to the products and services of Lionsoul Global Advisors is subject to eligibility requirements and the definitive terms of documents between potential clients and Lionsoul Global Advisors, as they may be amended from time to time.

The performance information shown is preliminary, unaudited, and based on internal estimates derived from the Fund’s accounting data. These results have not been independently reviewed or verified by the Fund’s Administrator and may be subject to adjustment.

Year-to-date (YTD) performance data are available upon request. Current YTD results do not materially differ from the performance figures shown herein, and any variances reflect customary timing and reconciliation processes.