Reports

Digital Asset Market: May in Review

Reports

Digital Asset Market: May in Review

Following a difficult stretch for digital assets marked by elevated volatility, thin trading volumes, and broad risk-off sentiment, May offered continued relief. Bitcoin reached a new all-time high of USD 112k, recovering the ground lost in April’s tariff-driven sell-off and extending gains into month-end.

As often seen in strongly consensus-driven markets, it didn’t take much for sentiment to shift. Heavy short positioning going into April created the conditions for a sharp reversal, which played out gradually across the month. While Bitcoin led the charge, altcoins began to catch up in May, though most still remain well below their prior highs.

Volumes remained light early in the rally, and many market participants were caught offside. Despite constructive regulatory and institutional news flow, broader positioning has stayed cautious. That said, improvement is visible. The futures curve is in contango, but the basis is still subdued versus past bull markets. As sidelined liquidity gradually re-enters the space and positioning shifts, the investment opportunity set for market-neutral strategies has begun to expand. This dynamic was already visible in May, and we expect it to continue improving into June.

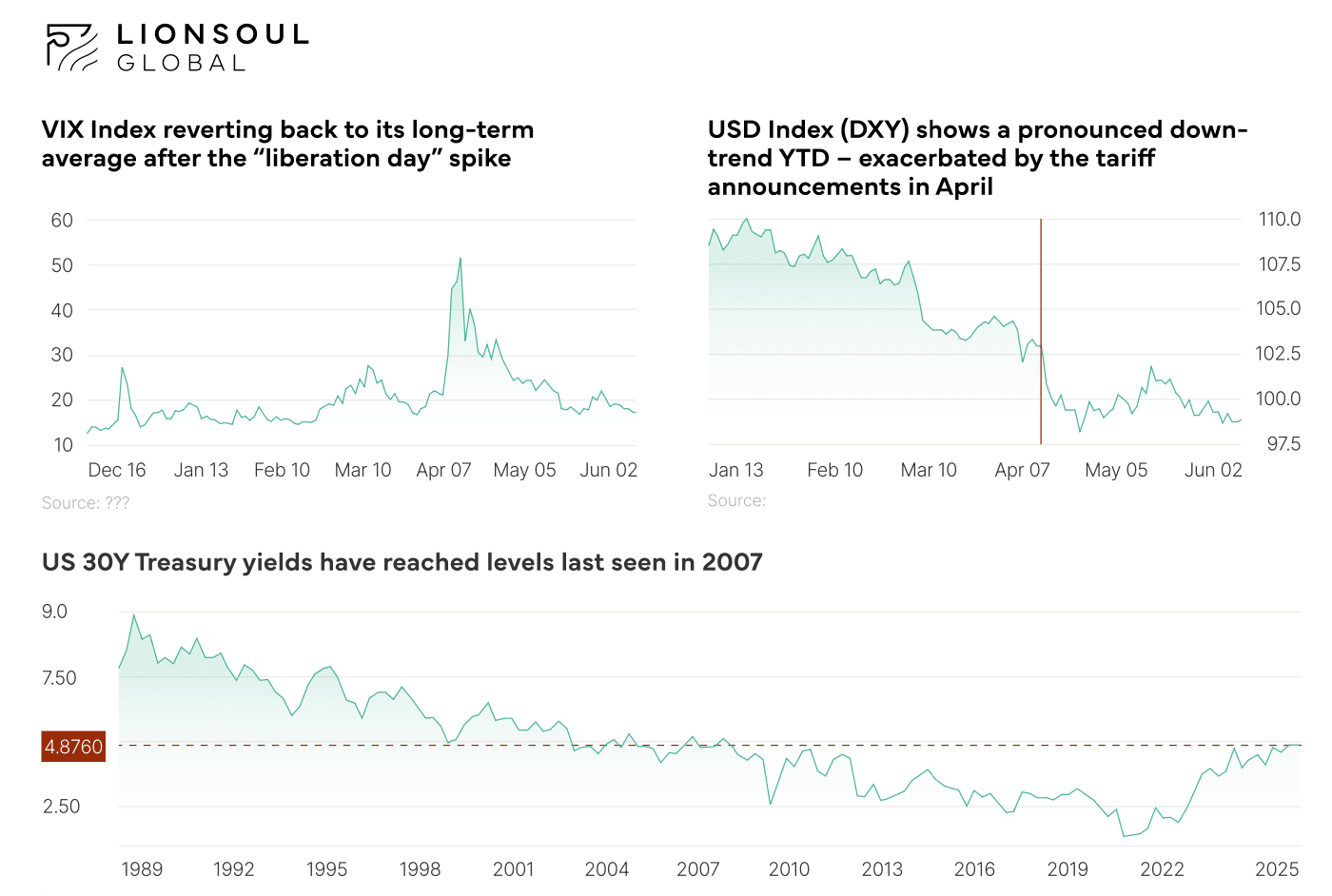

April’s “Liberation Day” tariffs triggered sharp moves across global markets, with particularly acute effects on U.S. Treasuries. The bond market reaction—spiking yields and disrupted liquidity—ultimately forced the U.S. administration into a partial reversal. A 90-day suspension and targeted exemptions helped ease concerns, and a subsequent federal court ruling declaring the tariffs unlawful offered further relief. The S&P 500 responded by rallying 6.1% in May, regaining lost ground and coming within reach of prior highs. European equities followed suit, with the DAX up 6.6% and EuroStoxx 50 up 3.9%. The VIX has retraced from its April highs and is now trading near its long-term average of 19–20, reflecting calmer conditions.

Meanwhile, the OECD cut its global growth forecast to the lowest level since the pandemic. U.S. GDP is projected to slow from 2.8% in 2024 to just 1.6% in 2025. Core inflation remains sticky, limiting the Fed’s room to manoeuvre. Rate futures now price in two cuts by year-end—down from three to four just a month ago.

While equity markets appear to have moved on from the tariff turmoil, it would be misguided to assume the episode won’t leave lasting consequences. The U.S. dollar has dropped ~4.3% YTD, and yields on 20- and 30-year Treasuries have risen above 5%—levels not seen since 2007. This reflects deepening unease over the U.S. fiscal outlook, especially with over USD 9 trillion in debt needing to be refinanced this year. Moody’s withdrawal of its AAA rating underscores these concerns.The abrupt imposition and subsequent suspension of tariffs have triggered deeper concerns about U.S. exceptionalism and the role of the dollar as a global safe-haven asset. Since the initial announcement, the U.S. Dollar Index (DXY) has declined by approximately 4.3% against a basket of major currencies.

U.S. 10-year Treasuries, traditionally viewed as a safe haven, have also lost some of their appeal—yields spiked to around 4.5% in the immediate aftermath and have remained elevated.

Of even greater concern is the sharp rise in longer-dated yields. The 20- and 30-year U.S. Treasury yields have both surged above 5%, with 30-year yields reaching levels last seen in 2007. This has amplified market anxiety around the long-term sustainability of U.S. fiscal policy, particularly against the backdrop of widening deficits and newly enacted tax cuts. The timing is problematic: the U.S. government must refinance roughly $9.2 trillion in debt—equivalent to nearly one-third of GDP— in 2025. Reflecting these concerns, Moody’s has withdrawn its AAA rating on U.S. sovereign debt, citing rising deficits and mounting refinancing risks.

Concurrently, the OECD has revised its global growth outlook downward to the lowest level since the pandemic. U.S. GDP growth is projected to decelerate sharply—from 2.8% in 2024 to 1.6% in 2025 and 1.5% in 2026. While the EU has managed to bring inflation below 2%, persistent core inflation in the U.S.—though easing—continues to constrain the Fed’s policy flexibility. Interest rate futures now price in two rate cuts this year, down from three to four just a month ago, as markets recalibrate following the tariff shock.

In summary, we see a growing disconnect between the deteriorating macroeconomic backdrop and the resilience of equity markets. While stocks have seemingly put the tariff episode behind them, further disruptions cannot be ruled out. In contrast, the bond market appears to be pricing in a more realistic assessment of the underlying risks.

Digital Assets: Bitcoin the Flagship

As noted in our last update, digital assets were not spared during the tariff-driven market turmoil, initially selling off alongside other risk assets. However, relative to their historical volatility, crypto markets held up surprisingly well.

While there is a clear disconnect between the grim economic outlook and the risk rally in traditional equities, the same cannot be said about digital assets. Most digital assets, especially layer-1 protocols, cannot be valued with the same metrics as traditional equities and hence there is a case to be made that they should trade less dependent on the overall macro picture. For Bitcoin on the other hand, there is a compelling argument to be made, that with increased user adoption, it will eventually live up to its promise as a genuine store of value as well as a macro and inflation hedge. While it is certainly too soon to settle the debate, it is fair to say that during these times of increased uncertainties, Bitcoin has fared relatively well and has even reached new all time highs on May 22nd.

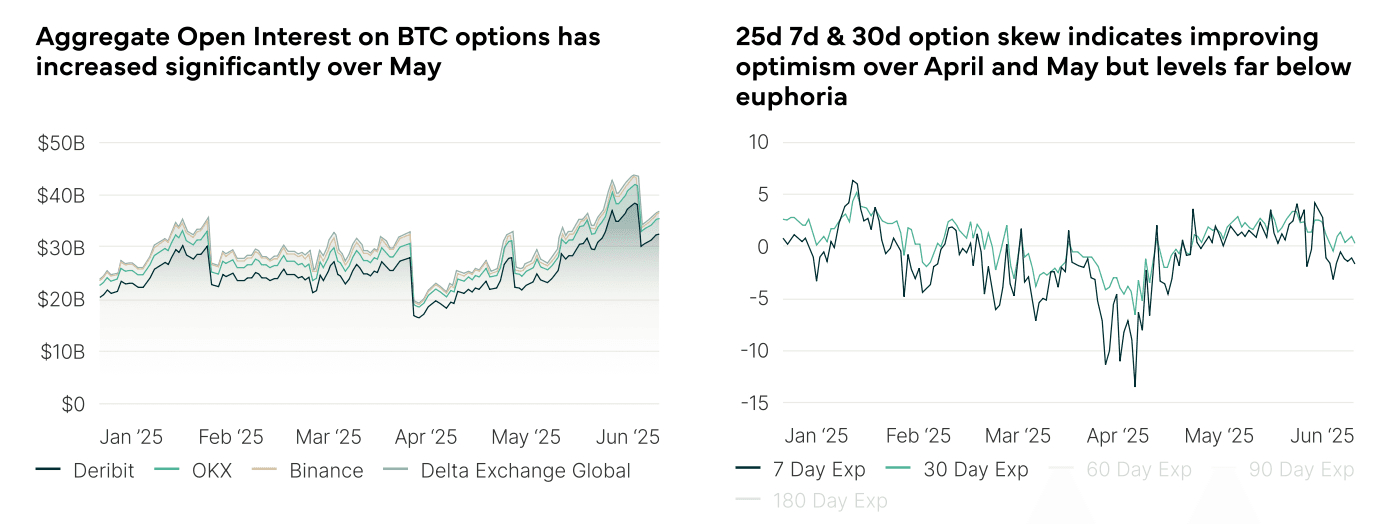

Early in the rally, price gains outpaced volumes, hinting at low conviction and under-positioned participants—what’s often referred to as a “hated rally.” But the tone shifted meaningfully over May. Total exchange volumes rose 14.8% month-over- month, Bitcoin futures open interest increased by 15.4%, and BTC options open interest surged 63%. Additionally, the 30- day 25-delta options skew indicates growing appetite for upside exposure, though sentiment remains far from euphoric.

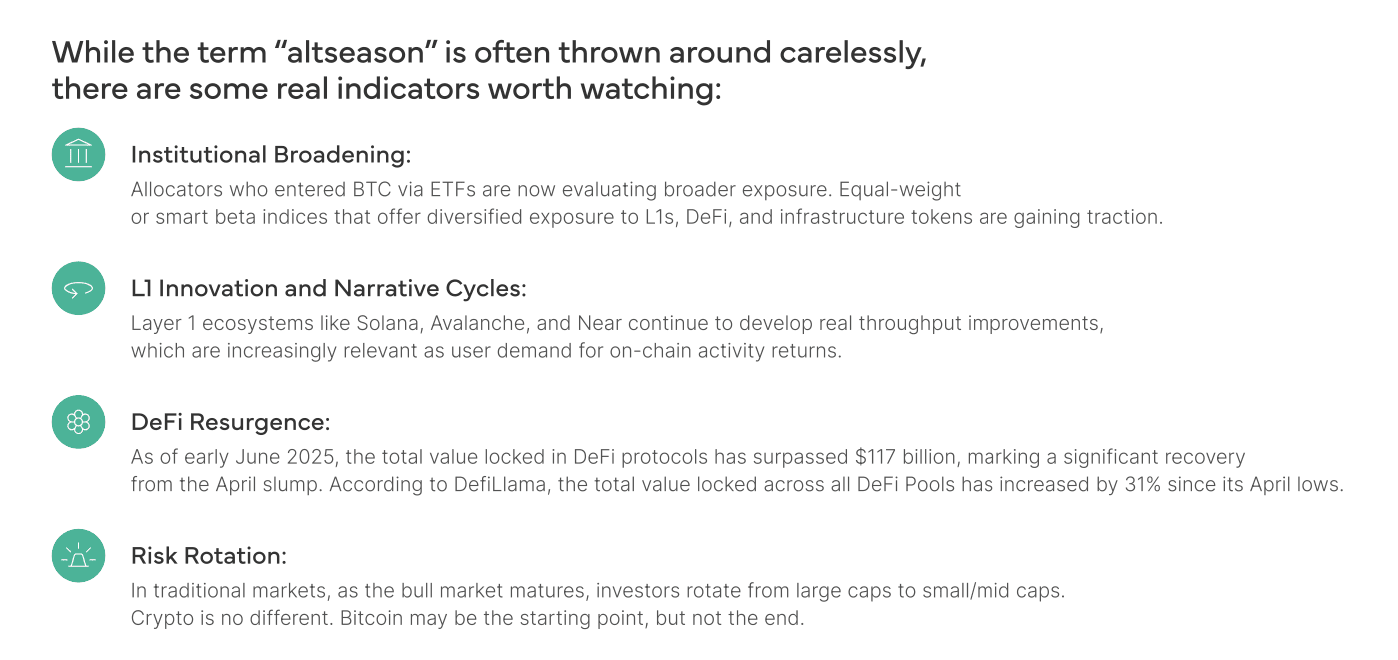

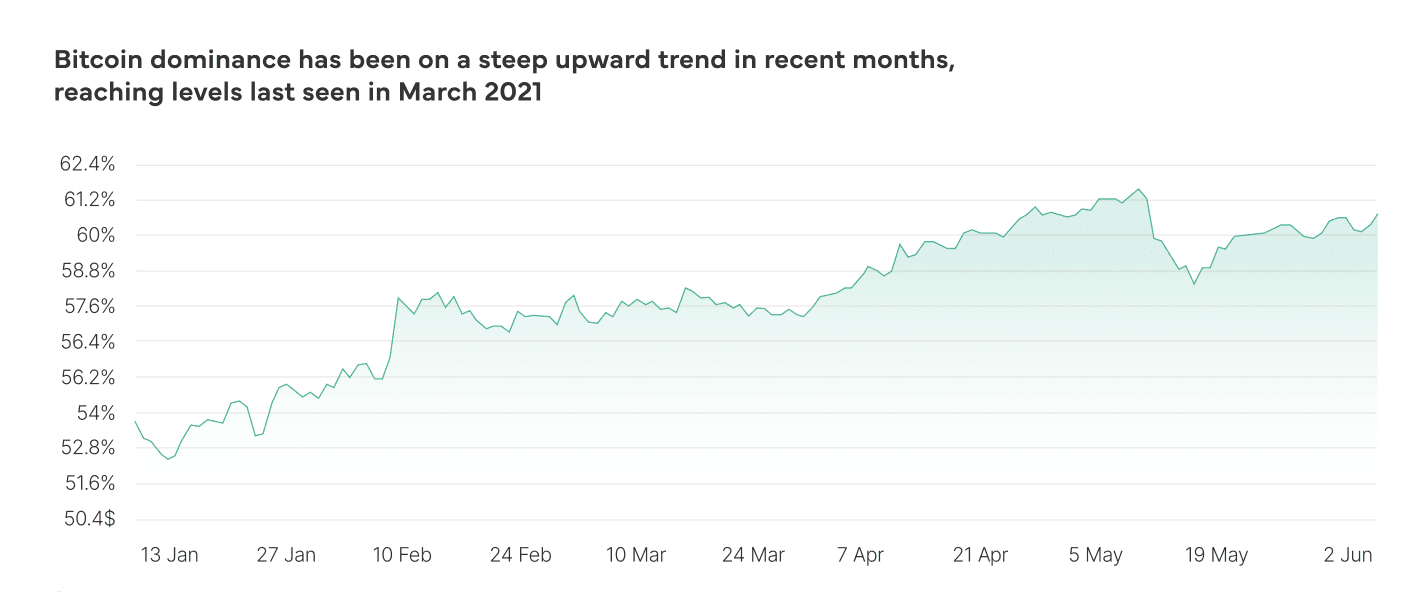

Bitcoin dominance — the percentage of total crypto market cap made up by BTC — has now climbed above 54%, up from ~38% in late 2022. Historically, BTC dominance peaks before altcoins begin to outperform. During the 2017 and 2021 cycles, altcoin rallies lagged the BTC all time highs by 2–6 months.

If history holds, the rotation from Bitcoin into altcoins may already be underway. Ethereum’s recent outperformance — posting an 81% rally since its April lows is a sign that the sentiment is starting to spill over from Bitcoin to the altcoin market.

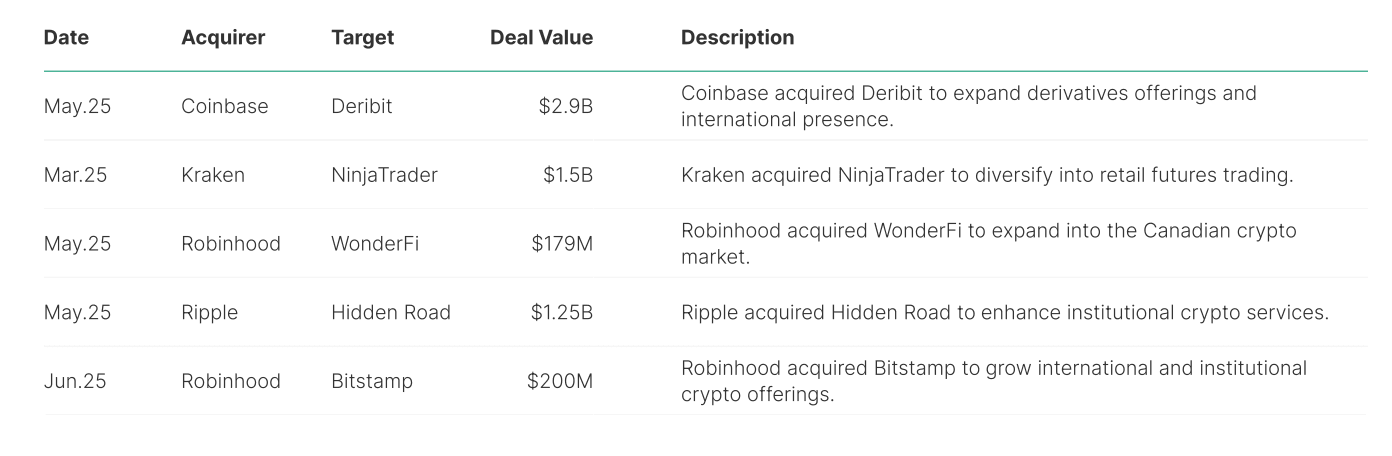

While traditional M&A markets remain subdued, consolidation in the digital asset space is accelerating. The pace and scale of recent deals point to a maturing market structure and growing institutionalisation across the sector. This wave of activity reflects both strategic expansion and a broader effort to professionalise core infrastructure.

We’ve compiled a detailed overview of the most significant recent transactions, highlighting how key players are positioning themselves for the next phase of growth.

Disclaimer

Investment advisory and asset management services are provided by Lionsoul Global Advisors LLC (“Lionsoul Global Advisors”), a U.S. investment adviser registered with the Texas State Securities Board (CRD #: 324883). Lionsoul Global Advisors is a member of the U.S. National Futures Association (NFA ID: 0553130). Information presented, displayed, or otherwise provided is for educational purposes only and should not be construed as investment, legal, or tax advice, or an offer to sell or a solicitation of an offer to buy any interests in a fund or other investment product. Access to the products and services of Lionsoul Global Advisors is subject to eligibility requirements and the definitive terms of documents between potential clients and Lionsoul Global Advisors, as they may be amended from time to time.