Insights

Digital Asset Market: April in Review

Insights

Digital Asset Market: April in Review

Following a challenging first quarter for digital assets, the second quarter began on similarly uncertain footing. Digital assets were swept up in the broader market turmoil triggered by sweeping tariff announcements, sold off alongside equities and bonds. Bitcoin fell roughly 10%, while many altcoins experienced even steeper declines. However, sentiment gradually improved over the month, and BTC ended April with moderate month-over-month gains.

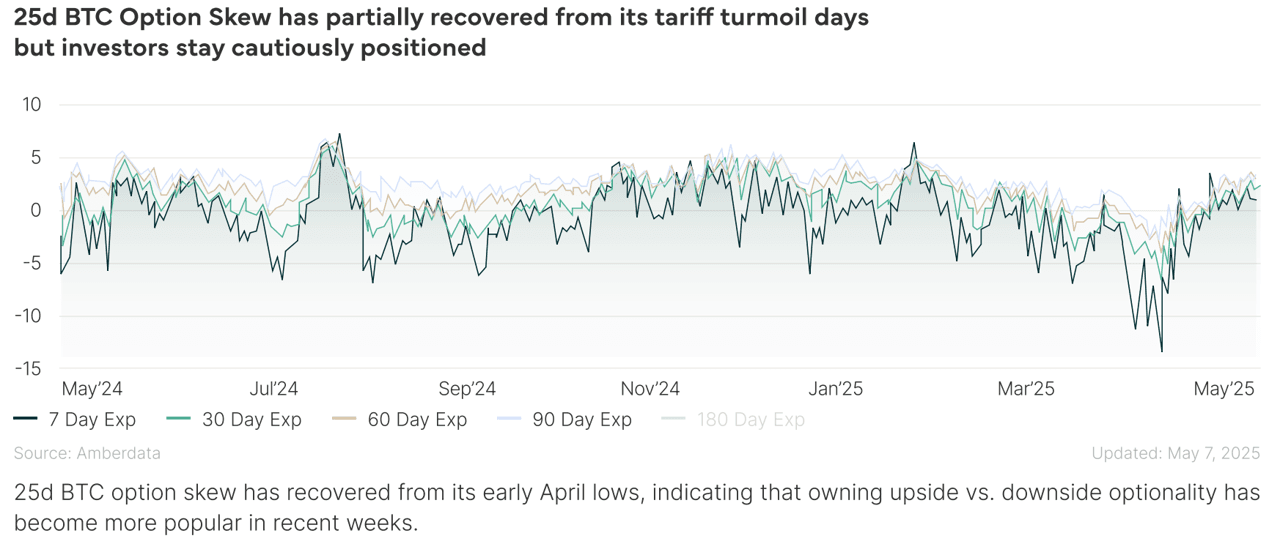

Despite this rebound, the environment remains cautious. Liquidity remains on the sidelines, and investor positioning is broadly conservative—dampening the opportunity set for market-neutral strategies.

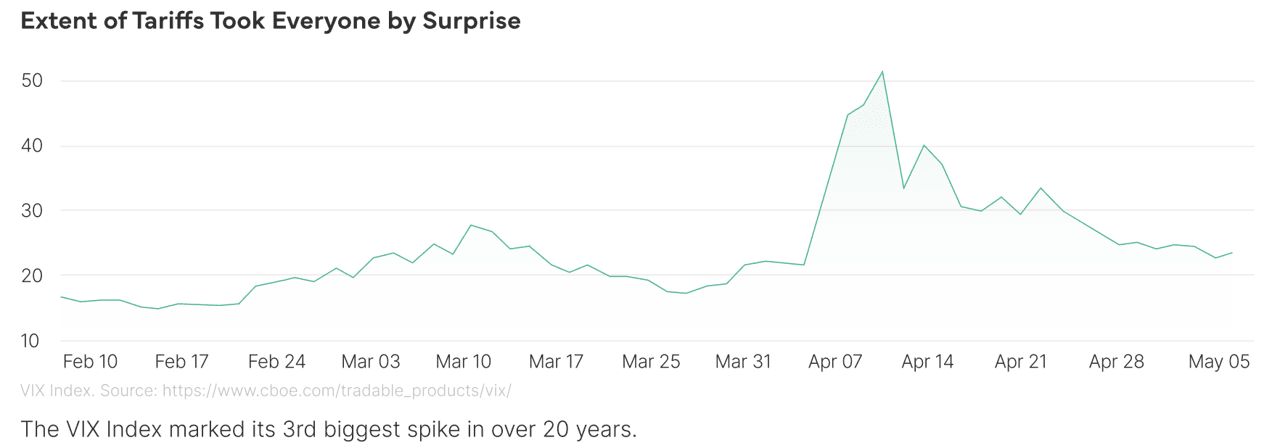

The highly anticipated “Liberation Day” announcements delivered a shock to global markets. While new tariffs were widely expected, the scale and unilateral nature of the measures—imposing weighted tariffs of 25–27%—far exceeded investor expectations. The VIX (the so-called “fear index”) recorded its largest spike since the onset of COVID-19.

The S&P 500 plunged 12% in the four days following the April 2 announcement, and nearly 19% from February highs—its worst drawdown since the pandemic. Globally, more than $5 trillion in market capitalisation was wiped out.

U.S. 10-year Treasury yields initially fell to 3.9% as investors fled to safety, but then reversed sharply to 4.5% by April 9—the steepest three-day rise since 1982. The simultaneous decline in stocks, bonds, and the dollar pointed to a deeper shift in sentiment and growing concerns around U.S. economic leadership.

Facing mounting market stress, especially in the Treasury market, the Trump administration announced a 90-day suspension of the new tariffs and began issuing wide-ranging exemptions. It also announced plans to begin formal trade talks with China in May.

Markets responded strongly. The S&P 500 logged a nine-day winning streak in early May, fully recovering from the “Liberation Day” crash. The Nasdaq surged more than 12% in a single session—its second-best day ever.

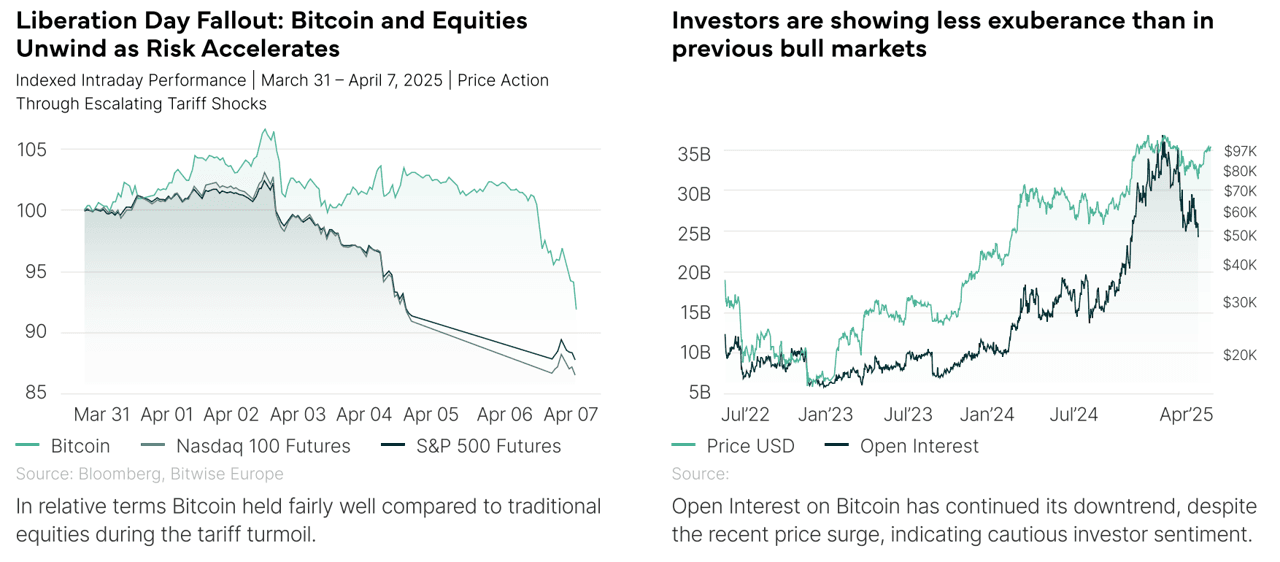

Crypto markets were initially caught in the crossfire, selling off in tandem with other risk assets. Yet relative to their historical volatility, digital assets held up reasonably well. Bitcoin rebounded sharply, reaching a monthly high of $97,800. However, sentiment remains fragile.

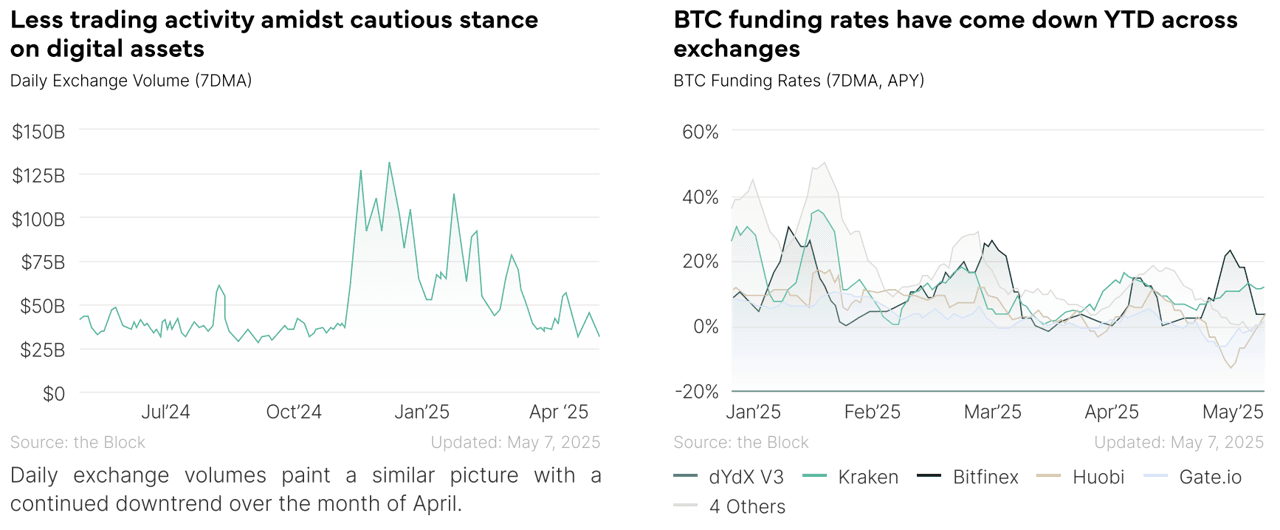

Trading volumes have lagged behind price gains, suggesting weaker conviction behind the move. Open interest has continued to drift lower, and BTC funding rates remain below their medium-term average. The futures curve is only slightly in contango, indicating muted demand for leverage and limited directional conviction.

This defensive stance has also limited opportunities for arbitrage strategies, including exchange, funding, and volatility arbitrage. In contrast to past bull cycles, investors appear more risk-aware and less exuberant.

While markets remain cautious, the policy backdrop for the crypto space improved in April:

1. The SEC dropped or paused over a dozen enforcement actions against crypto firms.

2. The Department of Justice disbanded its crypto enforcement unit, easing compliance fears.

3. Deribit, the largest option exchanges, is set to enter the US markets amid friendlier crypto regulations in the US.

4. Trump Administration Eases Tax Rules On DeFi Exchanges. U.S. President Donald Trump signed into law a bill to overturn a revised IRS rule¹ that defined DeFi exchanges as financial intermediaries.

5. Mastercard has announced a partnership with digital exchange Kraken² to allow investors to purchase goods and services using digital assets via Mastercard’s global payment network.

6. Stablecoin issuer and digital payment provider Ripple announced on April 8th its acquisition of multi-asset prime broker Hidden Road for $1.25 billion³.

7. The Central Bank of the United Arab Emirates (CBUAE) announced its plan to launch the digital dirham⁴ in the final quarter of 2025.